CoreWeave 4Q25 First Take.

The AI cloud unicorn's print this morning was mixed.1) On the positive side, growth met and slightly beat.

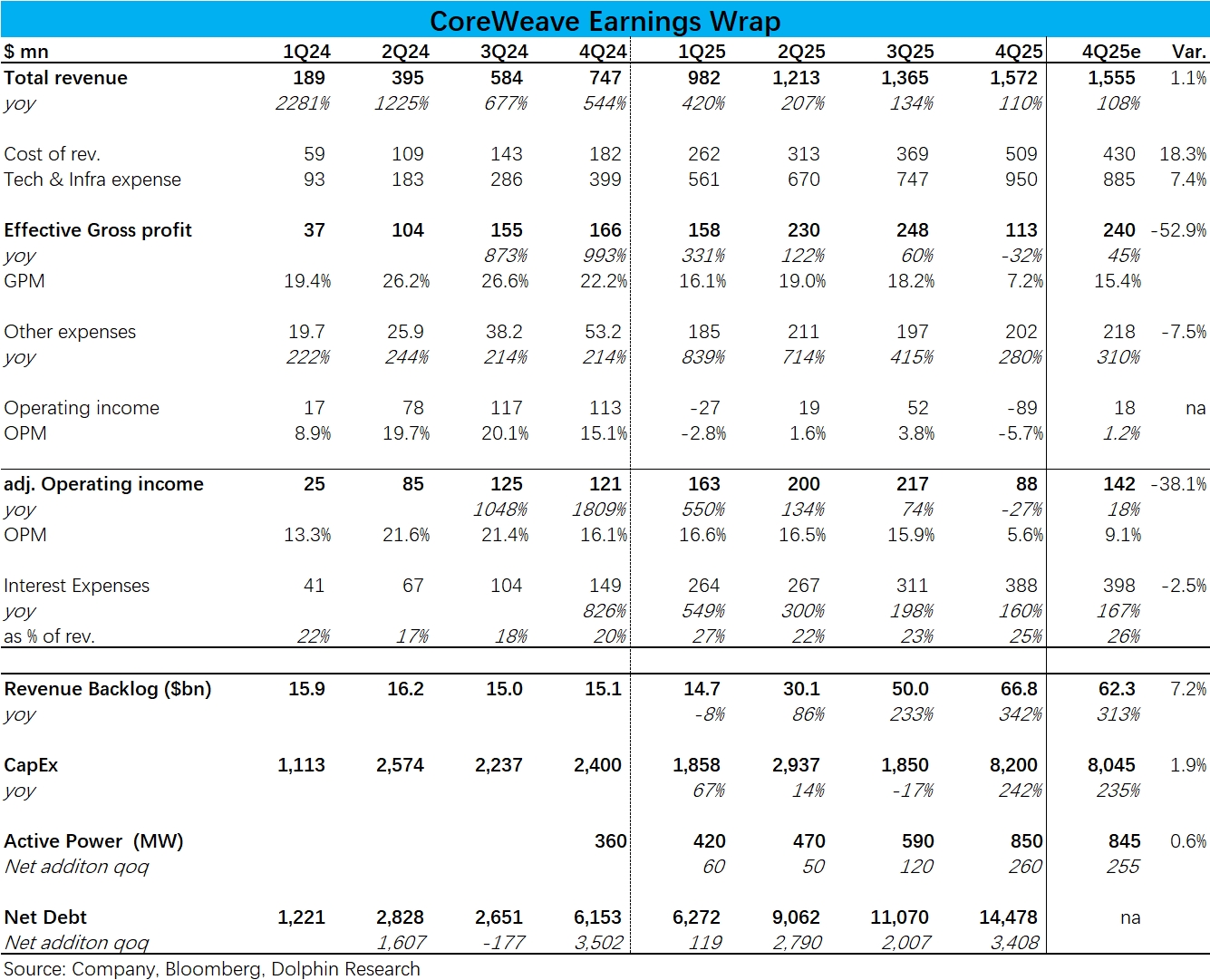

Revenue was approx. 1.57bn (+110% YoY), a touch above expectations.RPO reached 66.8bn, well above Bloomberg consensus of 62.0bn.Market had expected limited new contract additions this quarter given no announcements or chatter around mega-cap wins.

Actual additions still rose by ~17.0bn QoQ, not far off last quarter's ~20.0bn peak.While the company did not disclose customer names, the lack of rumors suggests non-mega-cap demand, potentially easing concentration risk.2) The negative: profitability badly missed.

With Capex and compute capacity ramping fast, 'true' GPM fell from 18% to just 7%, well below estimates.Adj. OPM was under 6%, versus already conservative market expectations of 8–9%.This indicates margin pressure during the compute ramp is far worse than anticipated.

Despite revenue doubling YoY, Adj. OP fell 27% YoY.3) Core operating metrics: total compute reached 850MW by quarter-end.

QoQ additions were 260MW, ~2.2x last quarter's increase, meeting market expectations.Supplier delays that slowed last quarter's go-live schedule did not cause further slippage.4) Correspondingly, Capex came in at 8.2bn, 3–4x prior quarters.

Newly online compute rose by ~2.2x.This confirms spend is running ahead of capacity coming online, pressuring margins.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.