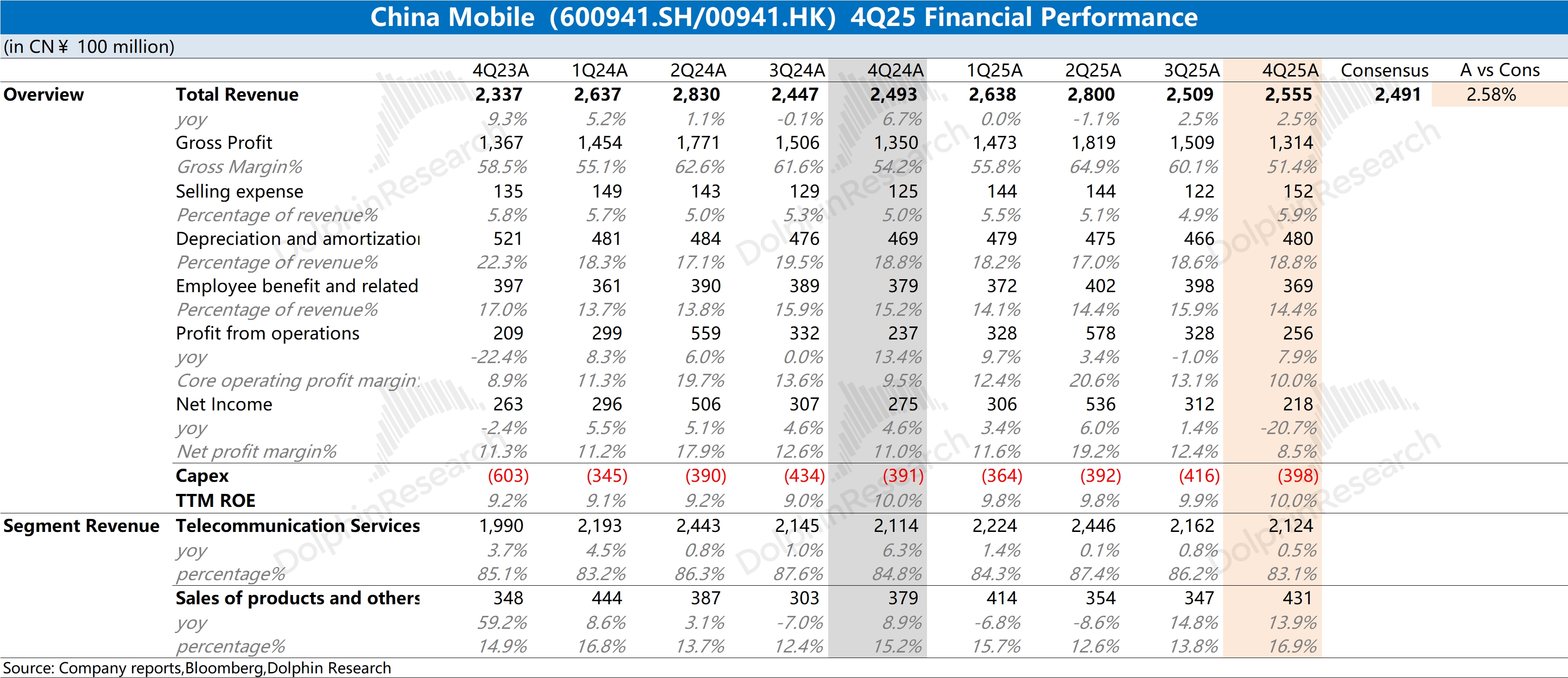

China Mobile 4Q25 First Take: Results were broadly in line with expectations, with revenue growth driven mainly by product sales while the core connectivity business posted a modest increase. Profit pulled back sharply on swings in other gains, while OP rose 8% YoY. By segment:

1) Data traffic kept the 'price cuts to drive usage' strategy, with Avg. unit price down 13% in H2 and mobile subs continuing to edge up.

2) Broadband grew around 8% in H2, with both subs and ARPU moving higher.

3) In other lines such as info services and product sales, growth was mainly driven by compute power services.

Beyond the steady operating metrics, the market is focused on the following. Key watch items are:

a) Capex: Quarterly capex was RMB 39.8bn, roughly flat YoY. Management guides 2026 capex at RMB 136.6bn, down 9.5% YoY. Within that, the company plans to trim communications network capex and keep increasing spend on the compute network (Approx. RMB 37.8bn).

b) Dividend: The company typically pays in Q2/Q3. Total dividends for 2025 are around RMB 103.4bn, implying a payout ratio above 70%.

Overall, China Mobile’s operating trends remained stable this quarter, while the decline in net profit was mainly due to other gains/losses. From 2026, a VAT policy change will reclassify data, SMS and MMS from 'value-added telecom services' to 'basic telecom services', lifting VAT from 6% to 9%.

With peak 5G investment behind, capex is on a downward trend and ROE is steadily improving, with the payout ratio staying above 70%. The higher VAT will weigh on near-term earnings, but over the medium to long term it remains a high-dividend pick. For more details, follow Dolphin Research. $CHINA MOBILE(00941.HK) $China Mobile(600941.SH)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.