BMNR Extreme Value Deduction 4.07

The focus for tracking BMNR this week remains on two main lines:

One is the Middle East conflict. It doesn't affect BMNR itself, but rather global liquidity and risk appetite. Although ETH rebounded back to 2.1k+ yesterday, the market is clearly still waiting to see if the situation will escalate further after the 48-hour deadline given by Trump tonight expires.

The other is the progress of the Clear Act. With Coinbase obtaining the OCC license and gaining federal-level trust bank/custodian status, Coinbase's negotiating stance on the issue of interest-bearing stablecoins may ease somewhat. The current market expectation is for a bank committee review on April 13th, which remains a key point affecting ETH's risk appetite and compliance narrative going forward.

BMNR officially announced its listing on the NYSE Main Board this week. Previously it was on NYSE American. This upgrade itself doesn't change the fundamentals, but it will increase the company's visibility, liquidity, and potential passive fund following space in the mainstream market.

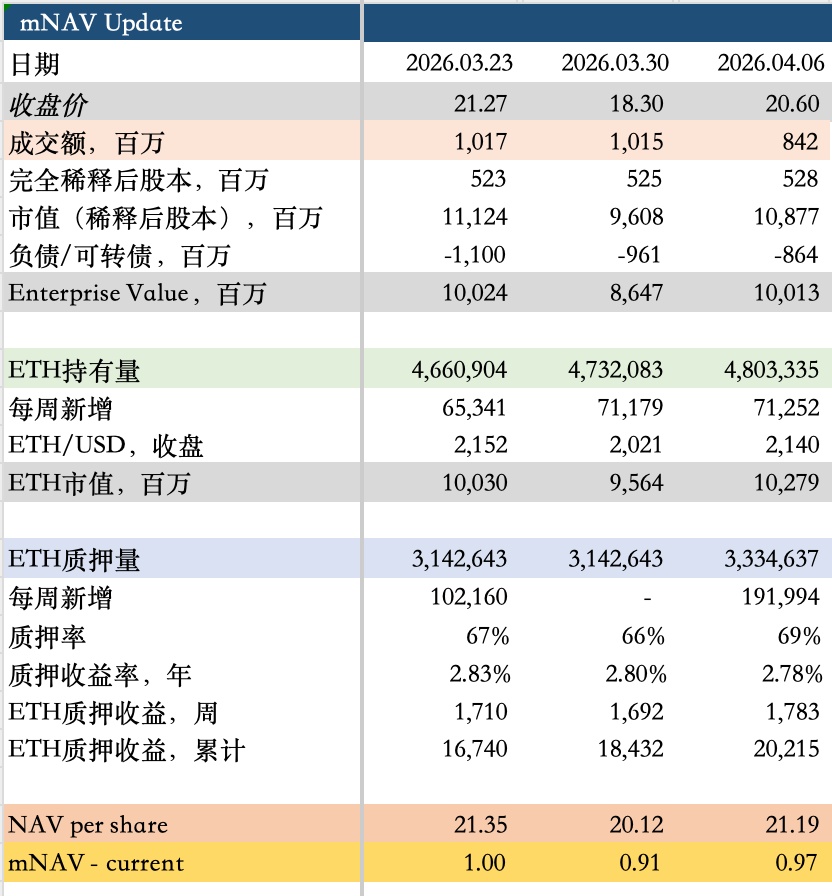

This Monday, BMNR updated its holdings to 4.8 million, with a new addition of 71,000 last week, achieving approximately 4% of ETH's circulating supply. Meanwhile, the cash position decreased to 860 million, continuing to be used for accumulating coins; with yesterday's overall crypto rebound, mNAV also recovered to 0.97.

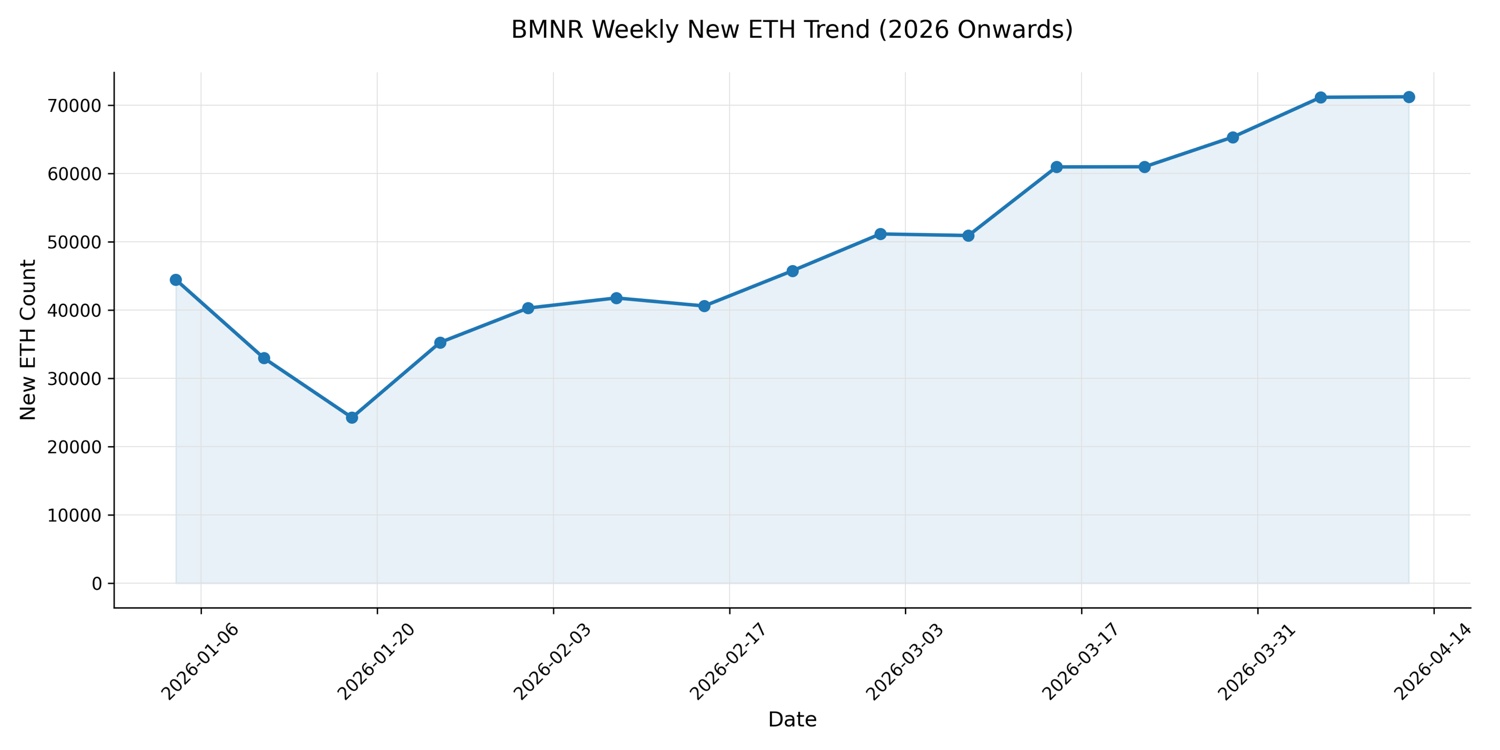

From the data, since entering 2026, BMNR has maintained weekly DCA while gradually increasing its purchase volume, from an initial 20,000 per week to the current 70,000. This is also one of the few sustained and resolute incremental buy orders for ETH in the current market. BMNR's staking volume has grown from 0 at the beginning of the year to the latest 3.3 million, accounting for about 70% of its total holdings. This means BMNR is gradually transforming ETH from a "holding asset" into a "yield-generating asset." Since actual staking rewards have already started in January/February, I am quite looking forward to the upcoming fiscal Q2 earnings report (December to February).

For this earnings report, I will focus on three things:

1. Whether staking rewards have begun to be disclosed separately.

2. Whether the related staking yield and cost rates are beginning to take shape.

3. Whether management has started to provide clearer guidance on third-party staking services.

Because for BMNR, what's truly important is no longer just "how much more ETH it bought," but whether the market will gradually believe it can expand from an ETH holding company to a staking platform infrastructure. Only if this step is established will BMNR's valuation system have a chance to transition from pure mNAV to mNAV + platform premium.

However, before ETH breaks through to 2.8k, it will still be difficult to obtain a higher premium. The current strategy remains to continue waiting, temporarily suspend extrapolating extreme ranges, and lie flat following ETH's fluctuations.

Not investment advice

$BitMine Immersion Tech(BMNR.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.