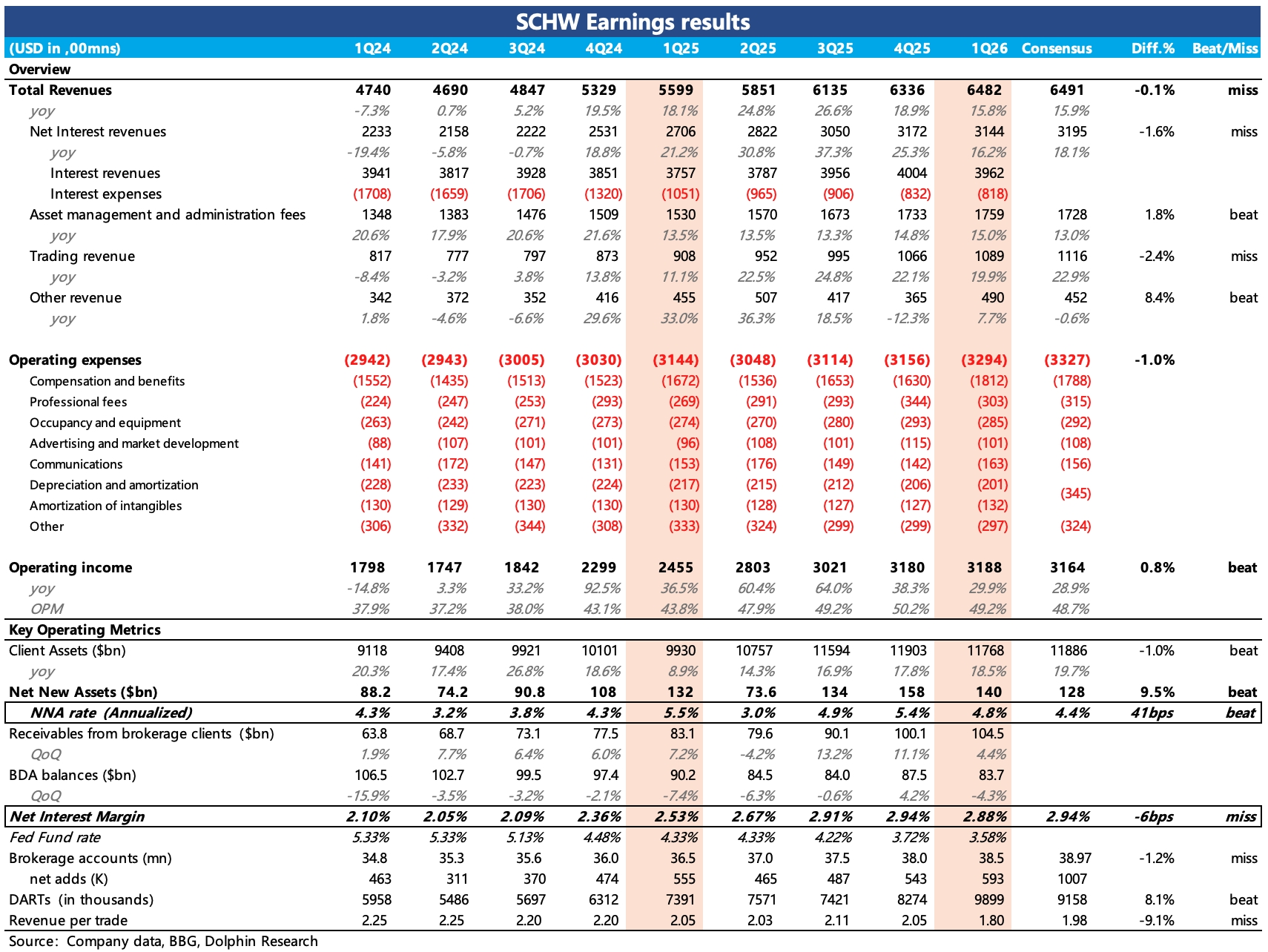

SCHW 1Q26 First Take: The quarter was solid, but expectations were high. Investors may focus on a slight revenue miss and a sequential dip in NIM.

After upbeat Feb metrics, management guided 16% Q1 revenue growth (vs. 14.5% then-consensus). That effectively raised the bar a month early.

1) Core metrics: NNA highlights brand strength; NIM likely saw short-term noise 1Q NNA was $140bn, which includes a planned $17.5bn outflow from mutual funds upon liquidation/maturity. Adjusted for that, the annualized growth rate was 5.3%, above the 5% full-year guide. In Mar, NNA growth reached 7.5% despite geopolitical noise.

Notably, core NNA here reflects the organic expansion of Schwab's legacy franchise. It excludes client assets associated with Forge Global.

NIM was 2.88%, down slightly QoQ. Interest income began to feel late-2025 rate cuts, while funding costs rose on higher short-term borrowings.

Margin balances are trending well; excluding RIA long/short strategies, platform user margin balances still rose 4% QoQ, outperforming the industry. Dolphin Research believes the uptick in short-term borrowings may be a tactical move to meet financing demand.

If so, this 'noise' should be viewed constructively over the medium to long term. Federal loans from the prior two years are being repaid in order, with less than $1.3bn outstanding at quarter-end.

2) Trading revenue +20%, DARTs +34% YoY (+20% QoQ), above expectations. Key drivers were a 6% increase in accounts, 12% higher assets per account, and a greater mix of derivatives trading YoY.

3) NII +16% YoY, high base and rate cuts in play. Interest-earning assets grew ~1%, and the YoY expansion was driven by wider NII spreads and a rapid run-off of short-duration debt that reduced interest expense.

4) AM up 15%, a steady Schwab hallmark. Total AUM, including money funds (funds + advisory), reached $4.3tn at quarter-end (+17% YoY), while the blended fee rate was unchanged.

5) Margin trajectory tempered by NIM and M&A. Operating margin was 49% in Q1, up sharply YoY but down 100bps QoQ, reflecting a small sequential decline in NIM and the Mar close of the Forge Global acquisition, with personnel expense up 11% QoQ.

6) Higher shareholder returns. The Q1 dividend was raised to $0.32/share (+19% QoQ). Buybacks totaled $2.4bn vs. $2.7bn last quarter, implying a current annualized yield of 5.7%—not rich, but not low either. $Charles Schwab(SCHW.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.