NFLX 1Q26 First Take: Shares sold off again on a guidance miss.

This came despite a quarterly beat that underscored management's typically conservative guide.

After NFLX walked away from acquiring WBD, investors expected a return to the playbook of price hikes plus efficiency.

The late-Mar US price increase further fueled hopes for a return to peak form.

However, margin guidance suggests investment will continue despite the deal being off.

New content spend will focus on games and live sports this year.

In detail:

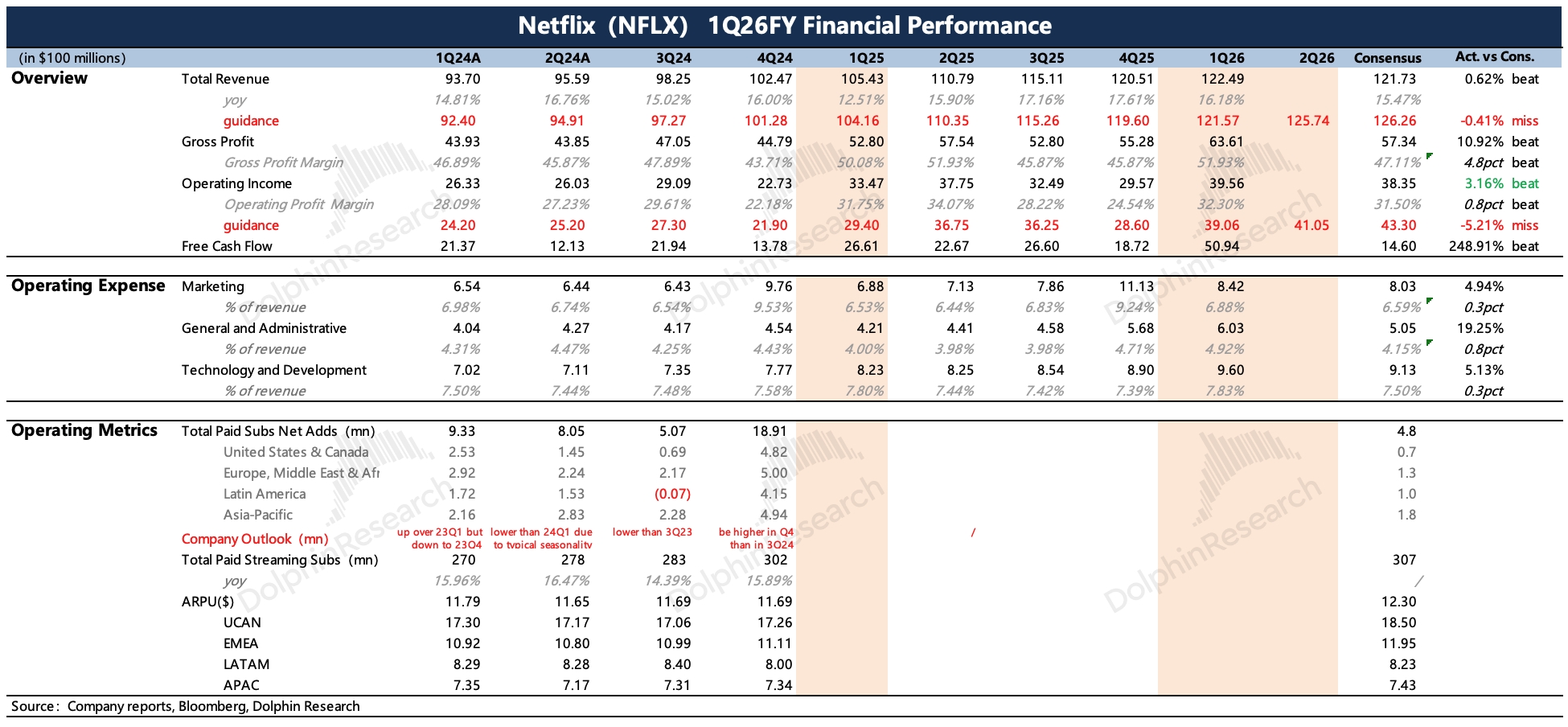

1) Is revenue growth set to slow? Q1 revenue was $12.2bn, +16% YoY (+14% cc), beating guidance.

We think the upside mainly came from sub scale and ads.

There were no broad price hikes in Q1; the late-Mar US move will fully flow into Q2.

Mgmt guides Q2 revenue to under $12.6bn, below consensus, implying growth slowing to ~13% vs. 16%, even with a 100bps FX tailwind.

Despite the Q1 beat and only a slight Q2 miss, mgmt did not lift the FY revenue guide, keeping $50.7–51.7bn.

That implies 12–14% growth on Jan FX, still assuming a 100bps FX tailwind.

That said, new monetization is ramping.

Mgmt expects ads to double to $3bn this year, and in early Apr it launched the standalone kids gaming app 'Netflix Playground', with more titles coming in 2026.

Games are meant to enhance member value and reduce churn, with limited direct revenue.

Even so, mgmt's revenue outlook still looks conservative.

2) Margin noise may slow the improvement? Q1 OP beat, with OPM up 50bps YoY.

The $2.8bn breakup fee from WBD was booked in other income.

However, Q2 margin guidance disappoints, with OPM below last year.

Mgmt cites content amortization tied to the kids gaming app. The acquisition of AI studio Interposition may also add personnel costs as integration progresses.

FY OPM guidance is unchanged at 31.5% (+250bps YoY).

But last quarter mgmt said the WBD deal would drag FY OPM by 50bps; after NFLX walked away, the Street had moved to ~32%.

3) Buybacks restart: Since the late-Feb decision to stop the deal, NFLX repurchased $1.3bn in Q1, with $6.8bn remaining under the current authorization.

The $2.8bn cash compensation improved liquidity, and FY FCF guidance was raised to $12.5bn from $11bn (the breakup fee is taxable).

Content spend was $4.8bn in Q1 (+21% YoY), with FY content investment near $20bn.

Some investors worry higher content amortization could cap OPM improvement. $Netflix(NFLX.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.