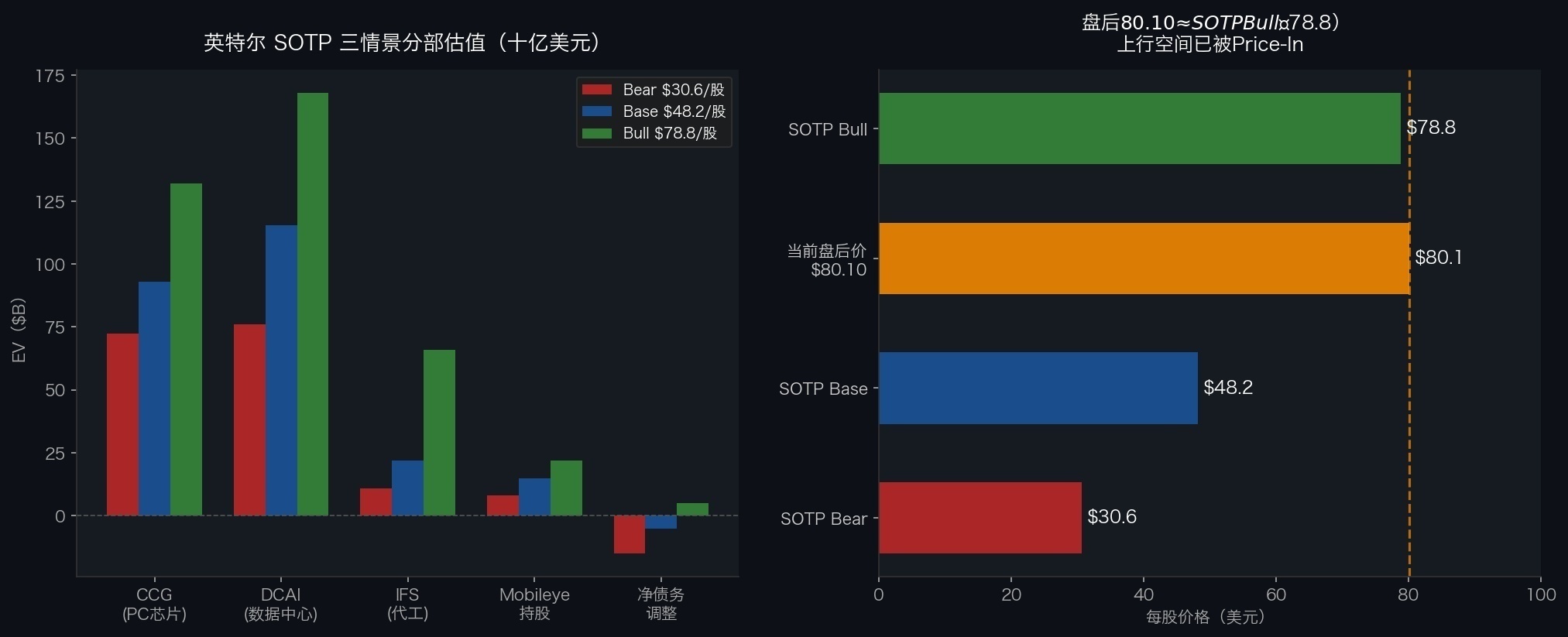

$Intel(INTC.US) There's also a kind of unorthodox algorithm that I'm not sure is reasonable,

which involves taking the 2027E fiscal year revenue guidance. If, from a foundry platform perspective, it aims to match TSM's forward P/E level, assuming it can achieve TSMC's 41% (5-year average) profit margin level,

then the market cap would roughly reach 59.69 billion * 20 P/E * 41% = 489.5 billion. Converted, that's about $98 per share, which is on par with the current highest price target of $95 from HSBC.

This is similar to how AMD is benchmarked against NVDA, and Marvell Technology is benchmarked against Broadcom.

涨到$80,但估值框架变了——英特尔的底牌是什么

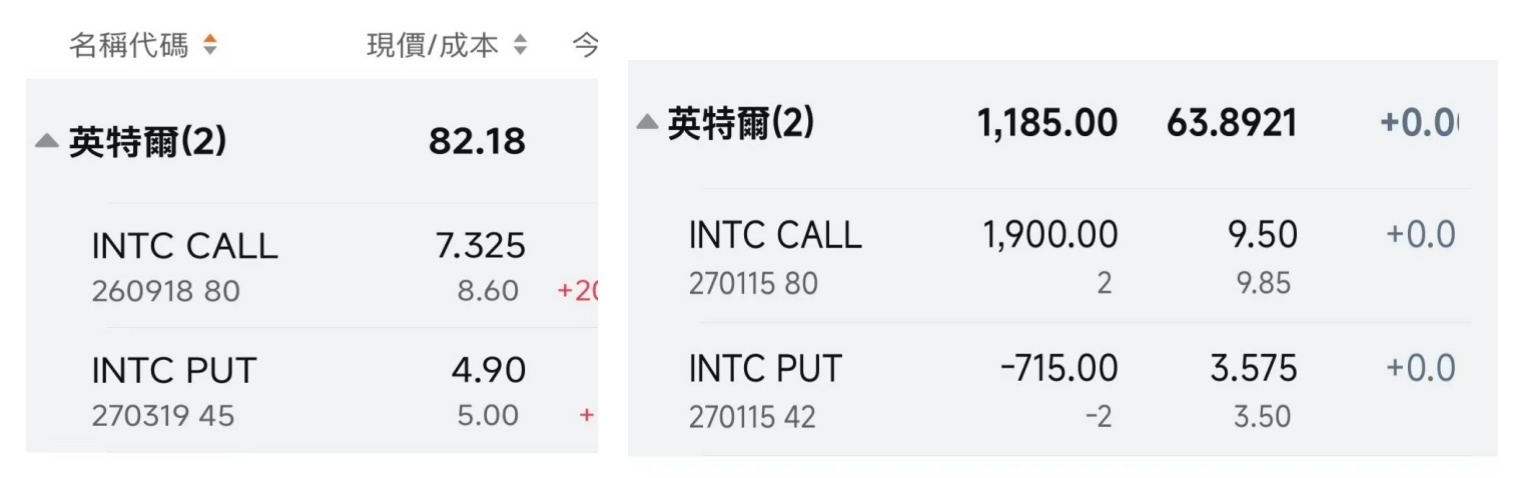

1、一觉睡来,50 家分析师的目标价全部过时了先说发生了什么。4 月 23 日盘后,英特尔发布了 2026 年第一季度财报。数字很漂亮:营收 +7.2%,每股收益、毛利也大超预期,DCAI 业务表现亮眼,营收 51 亿美元,跨季度破两位数增长 +22%,同时,公司给出强劲二季度指引$13.8-14.8B ,中值 $14.3B,远超华尔街 $13.1B 然后发生了一件有意思的事...

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.