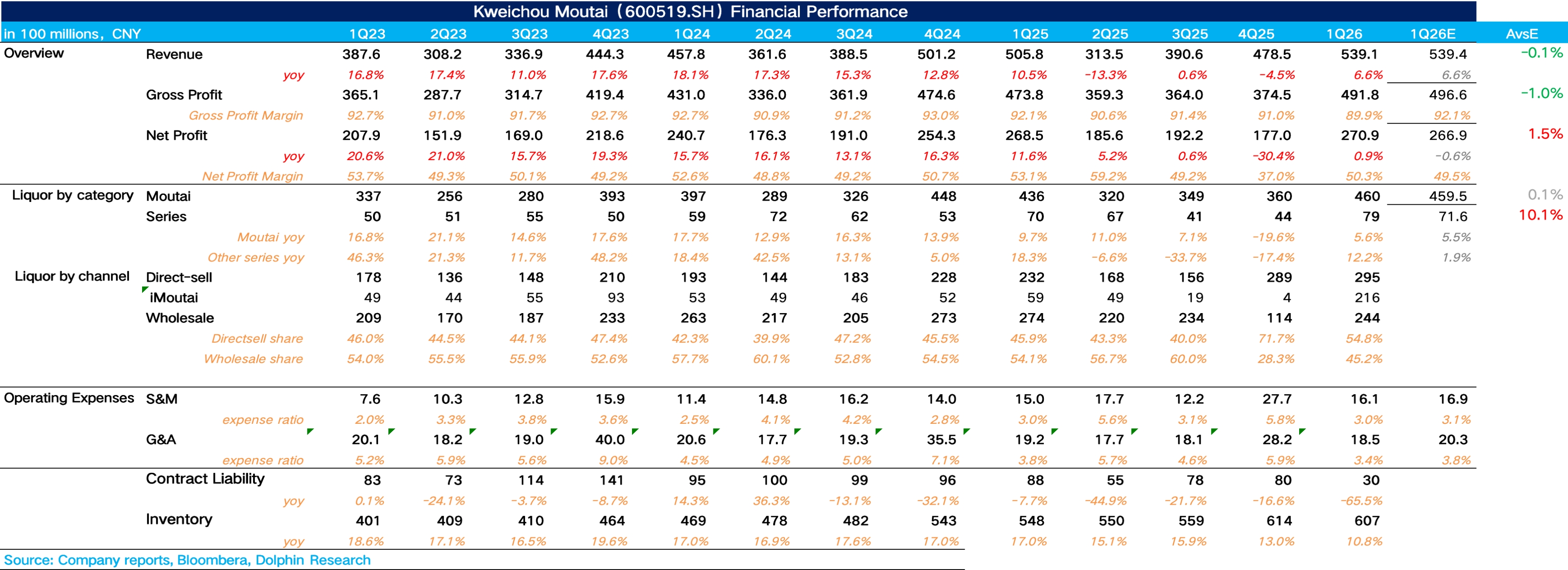

Moutai 1Q26 First Take: As the first print since channel reform took effect, results looked solid, with revenue returning to growth despite a high base last year. The only blemish was profit growth lagging revenue as non-standard SKUs saw price cuts and a reduced mix.

Moutai delivered total revenue of RMB 53.9bn (+6.5% YoY), with Feitian Moutai at RMB 46.0bn (+5.6% YoY). With iMaotai contributing the core incremental gains, we infer Feitian has reclaimed the growth baton. By contrast, non-standard SKUs — premium, zodiac and vintage lines — were overpriced last year and channel-heavy, resulting in widespread price inversion amid weak demand, so we expect light allocation and muted growth in Q1.

Series liquor generated RMB 7.9bn, down 12.2% YoY. After two quarters of clean-up in Q3–Q4 last year, growth is set to normalize back to double digits. We think 1935 remains the key support, while mass-market sub-brands such as Prince and Yingbin focus on stable inventory and price discipline in a soft demand environment.

By channel, direct sales reached RMB 29.5bn in 1Q26 (+27% YoY). iMaotai delivered RMB 21.6bn, accounting for 73% of direct sales. This underscores iMaotai’s shift from an auxiliary outlet for non-standard SKUs to the core carrier of Moutai’s To-C strategy.

GPM fell 220bps to 89.9%, as price cuts and reduced allocation for non-standard SKUs drove an unfavorable mix. Opex was broadly flat YoY, delivering attributable net profit of RMB 27.2bn (+1.5% YoY). See Dolphin Research’s upcoming earnings take for more details.$Moutai(600519.SH)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.