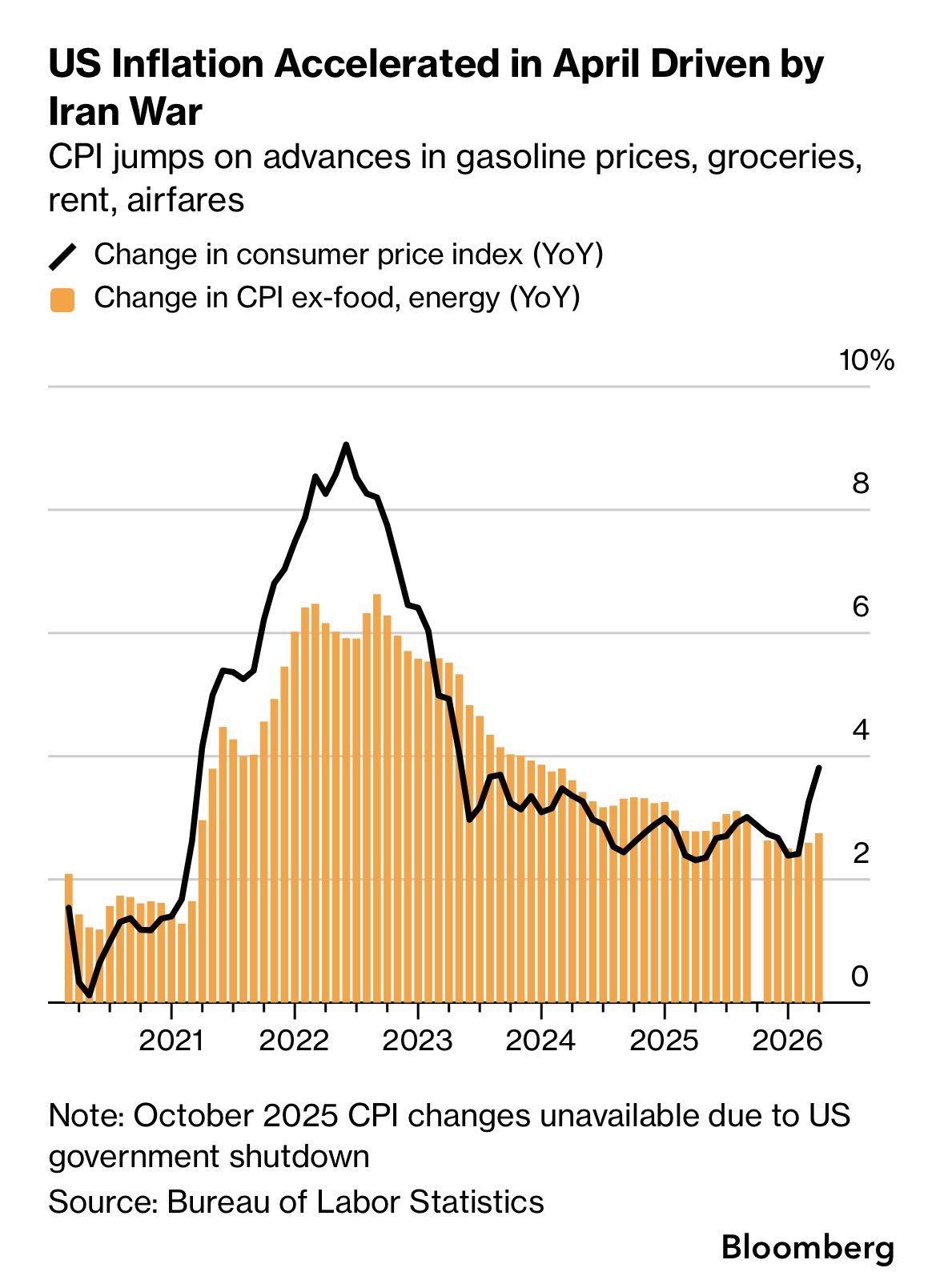

The real problem may not be inflation

When the market saw "US April inflation exceeded expectations" today, its first reaction was: rate cuts are off the table.

Breaking down the data reveals that this inflation episode is not as bad as the market imagined.

Combined with Bloomberg data, the current situation looks more like a "war-driven disruption" rather than a new round of a comprehensive inflation cycle.

· The most crucial information from the data is actually:

Headline CPI suddenly picked up, but core CPI did not explode in sync.

This means: the main issue with this inflation is not "overheating demand," but energy and some short-term disruptions.

① Energy Data

· April energy inflation MoM +3.8%

Although still high, compared to March's +10.9%, it has clearly cooled down.

The reason the market is sensitive is essentially still because of:

· Iran war risk

· Surging crude oil prices

· Gasoline price pass-through

· Rising jet fuel prices, which is a typical case of "geopolitical imported inflation."

In other words: this is not the US economy overheating again, but oil prices "adding drama" to CPI.

② Food inflation is high, but the problem is not systemic

· Food inflation MoM +0.5%. The most obvious are: beef, eggs, fish, chicken. This part is actually related to global supply chains, feed, and transportation costs.

Against the backdrop of war: energy → transportation → agricultural product prices will form short-term transmission.

The problem is: food and energy are inherently the most volatile parts of CPI. What the market truly cares about is core inflation.

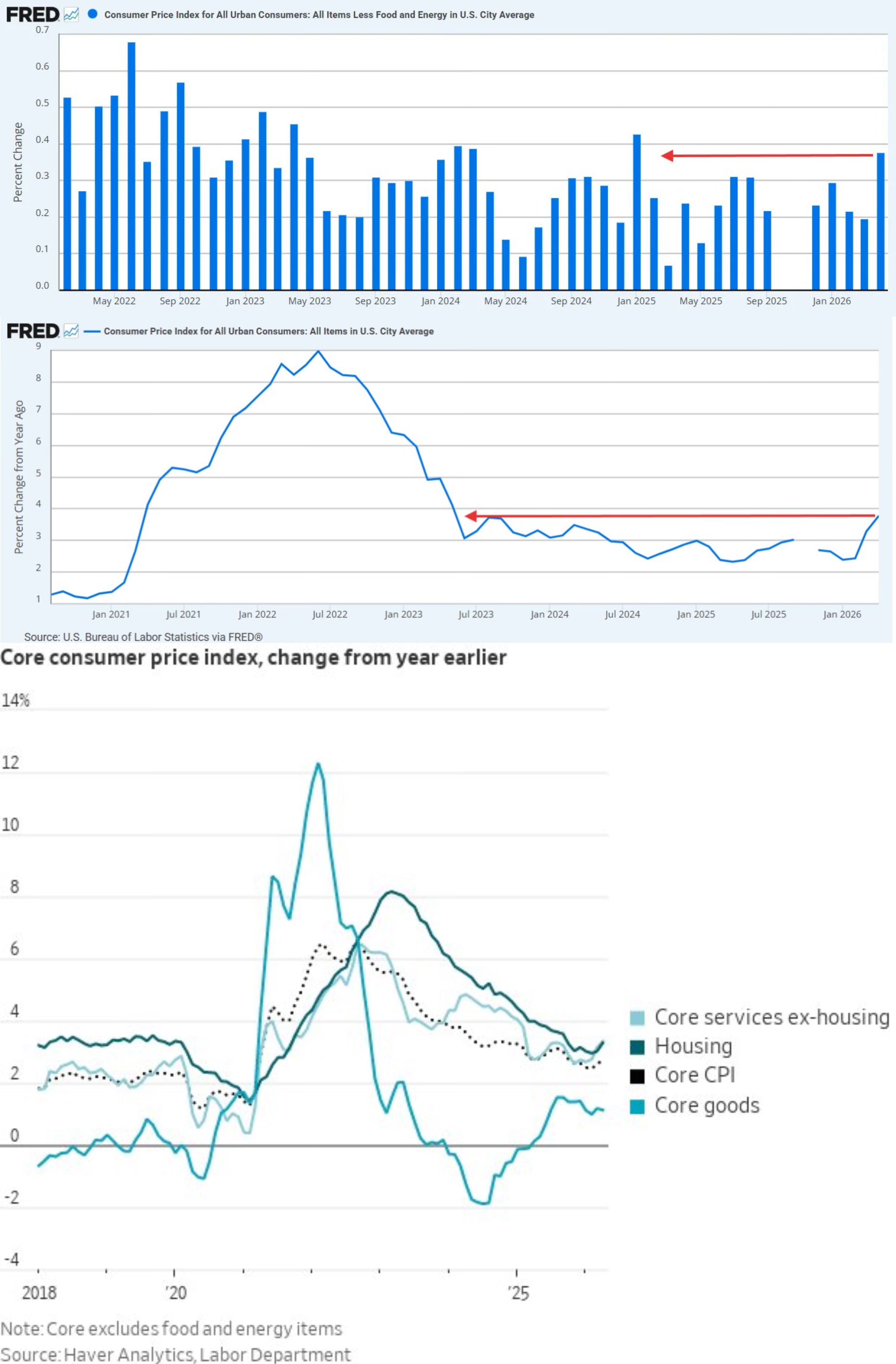

③ The real key: Core goods inflation is not bad

· Goods inflation MoM 0%

· It was still 0.1% in the previous two months

This means: US consumer goods demand has not gone out of control again.

If the economy overheats for a second time, the first to blow up are usually core goods. For example: cars, home appliances, consumer electronics, durables.

This indicates: the current US economy looks more like "localized price increases" rather than a full-blown inflation spiral.

④ Other service data

· Medical care services: 0%

· Education services: 0.2%

· Recreation services: 0.1%

· Transportation services: 0.3% (significantly better than March)

Truly widespread service inflation has not gotten out of control. This is completely different from the level seen during the 2022 comprehensive inflation state.

⑤ The market's real reversal point also explains everything

If this inflation really "exploded," theoretically we should have seen:

· 2-year Treasury yield surging

· US stocks continuing to dive

· Rate cut expectations being pushed back significantly

But the actual movement was: after the 8:30 data release, the 2-year rate first went down, and US stocks first went up. This shows that the market initially considered the data "acceptable."

The real reversal happened after 8:42.

This means: the market decline is more likely due to sentiment trading, positioning issues, AI profit-taking at highs, and a short-term stampede in risk assets, rather than simply because inflation is out of control.

The April CPI data is essentially more like a war-type inflation disruption, not the economy overheating again.

What really needs to be watched now is actually:

· Whether oil prices will continue to surge

· Whether future rent data will be revised

· Whether core services inflation will pick up again

If the latter two items fall back again, then this inflation data is likely just the market "seizing on an excuse" in a high-valuation environment.

Data source: Bloomberg

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.