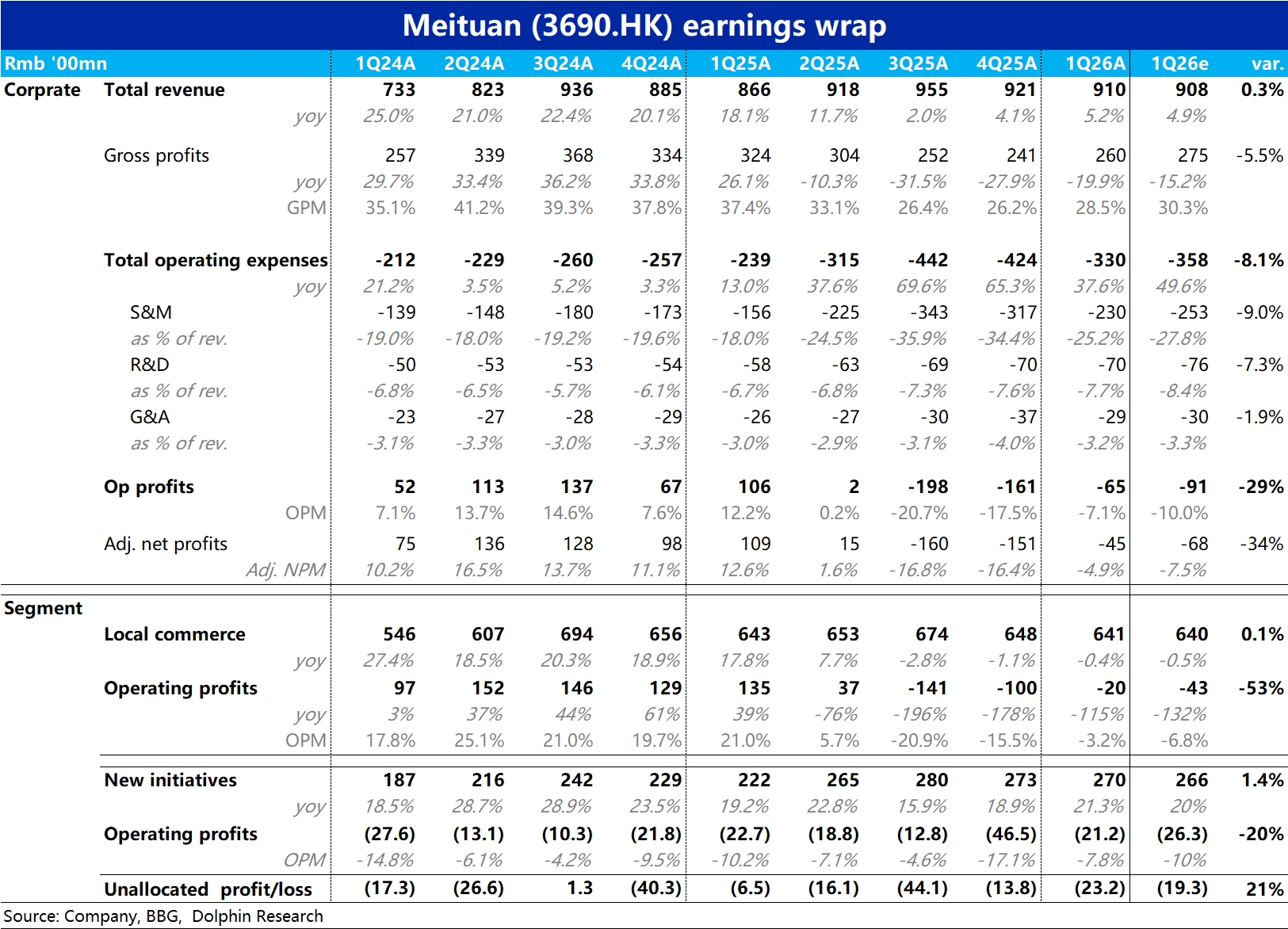

Meituan 1Q26 First Take: Results were not strong in absolute terms, but beat expectations, driven by faster-than-expected loss narrowing in Core Local Commerce.

Key points:First, management made minor tweaks to reporting definitions and restated historical data (our charts still follow the old series, so there may be small gaps vs. the latest disclosure).

Key changes: commission and advertising were unified under merchant services revenue, and first-party retail was carved out from 'other' and disclosed separately.Implications include: a) it will be harder to parse the performance of to-home vs. in-store businesses from reported data, increasing reliance on color from small-group calls; b) carving out first-party retail allows better tracking of Xiaoxiang Supermarket's growth.

Total revenue was approx. RMB 91bn (+5% YoY), a slight acceleration vs. last quarter and broadly in line.

Notably, operating loss came in at ~RMB 6.5bn, well below Bloomberg consensus of ~RMB 9.0bn.By segment, revenue for Core Local Commerce and New Initiatives was broadly in line with expectations.

The surprise was on profitability: Core Local Commerce posted only ~RMB 2.0bn in operating loss, well below the Street's >RMB 4.0bn.

Dolphin Research believes most of the beat came from the to-home (on-demand delivery) business.

Our initial estimate puts Meituan's per-order loss at ~RMB 1.0–1.1 this quarter, better than the market's ~RMB 1.4. This implies the UE gap vs. Alibaba Flash Delivery widened from ~RMB 1.6 last quarter to ~RMB 2.0.Losses in New Initiatives were also smaller than expected, narrowing to ~RMB 2.1bn vs. RMB 4.65bn last quarter.

According to the company, domestic first-party retail and overseas operations both improved, and seasonality (Q1 being a lighter investment and profit-rich quarter) also helped. However, higher AI spend lifted unallocated losses; looking at New Biz + Unallocated together, the total loss was not far from expectations.On costs and expenses, with revenue growth broadly in line and no clear acceleration, loss narrowing mainly reflects lower subsidies and related spending.

Marketing expense was RMB 23bn, well below the market's RMB 25.3bn, explaining most of the profit beat.

Overall, the to-home business is narrowing losses faster than expected.

There are also market rumors that parts of 2Q turned profitable in certain time windows, a positive marginal trend.However, investor focus has shifted to in-store competition with Douyin. Given limited disclosure in the FS, watch for color on the upcoming small-group call. $MEITUAN(03690.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.