Global Stock Market Review for the First Half of 2026: AI and Hardware Tech Lead the Way, Finding New Opportunities Amid Divergence

In the first half of 2026, major global stock markets showed a clear divergence. As of June 30, 2026, the S&P 500 in the US rose by 9.6%, the Nasdaq 100 by 20.0%, and the Dow Jones by 8.6%, with their performances diverging significantly, primarily driven by the technology and AI-related sectors. The Nikkei 225 performed remarkably, accumulating a gain of over 35.2% in the first half, benefiting from the strength of the semiconductor equipment sector. South Korea's KOSPI index, propelled by the memory "super cycle," surged by a staggering 96.7%, standing out exceptionally.

The performance of the Hong Kong stock market was relatively weak. As of June 30, 2026, the Hang Seng Index fell by 10.7% in the first half, and the Hang Seng Tech Index dropped by 18.9%. Overall, global stock market trends diverged significantly, but the investment theme was highly consistent: capital continued to flow towards the AI hardware technology sector, with the semiconductor field becoming the biggest highlight. In contrast, software and SaaS stocks, as well as platform economy stocks, saw significant valuation adjustments due to substitution concerns brought about by the widespread adoption of AI Agents.

(Source: Bloomberg, performance data excludes exchange rate factors and is calculated in local currencies.)

AI Hardware Technology, Especially the Semiconductor Sector, Leads the Gains

As seen from global stock market performance, the core driver in the first half of 2026 remained AI-related hardware technology. According to Bloomberg data, as of June 30, 2026, the Philadelphia Semiconductor Index surged by 101% in the first half, and the Solactive Asia Semiconductor Select Index also rose by 97.6%, fully reflecting the extremely strong demand from investors for AI infrastructure in both the US and Asian markets.

Among these, the memory sector performed most prominently, benefiting from the explosive demand for DRAM and NAND storage from AI data centers. Related companies like SanDisk and Micron saw their stock prices soar significantly. This directly explains the exaggerated gains of South Korea's KOSPI, with memory giants like Samsung and SK Hynix being the main contributors. The Japanese stock market, due to its high proportion of semiconductor equipment and material supply chains, also saw strong performances, such as from Tokyo Electron.

Software Stocks Under Pressure, Dragging Down US and Hong Kong Markets

In stark contrast to hardware technology, software and platform economy stocks were generally under pressure. In the US market, heavyweight stocks like Microsoft and META fell against the market trend, limiting the overall gains of the S&P 500 and Nasdaq. Investors are concerned that new technologies like AI Agents will accelerate the replacement of traditional SaaS applications, putting pressure on the valuations of some software stocks. For example, PLTR fell by 34.4% in the first half as of June 30, 2026.

The performance of the Hong Kong stock market was even worse, mainly because the platform economy is no longer the market focus. Software and internet stocks like ATMXJ (Alibaba, Tencent, Meituan, Xiaomi, JD.com) as well as NetEase and Baidu, which have significant weightings in the Hang Seng Index and Hang Seng Tech Index, became the main drag factors. However, the hardware technology sector in Hong Kong performed strongly against the trend. SMIC rose by 25.1% in the first half as of June 30, 2026, and companies like Hua Hong Semiconductor, Hongli Semiconductor, Kingboard Laminates, Lenovo Group, and ASMPT all hit record highs, indicating that capital is concentrating on hardware technology with physical manufacturing and AI infrastructure attributes.

(Source: Bloomberg. All performance data as of June 30, 2026. US stock data in USD, Hong Kong stock data in HKD.)

Summary: AI Agents Drive a New Growth Cycle

Summarizing the investment environment in the first half of 2026, the market focus remains firmly locked on technology leadership, especially the emergence and widespread application of AI Agents. The market generally anticipates that AI technology will significantly enhance the overall efficiency of the economy, bringing about productivity leaps and multiple synergistic effects. In contrast, traditional SaaS stocks continue to be under pressure due to concerns about "being replaced by AI."

(Source: Stanford AI Index Report 2026)

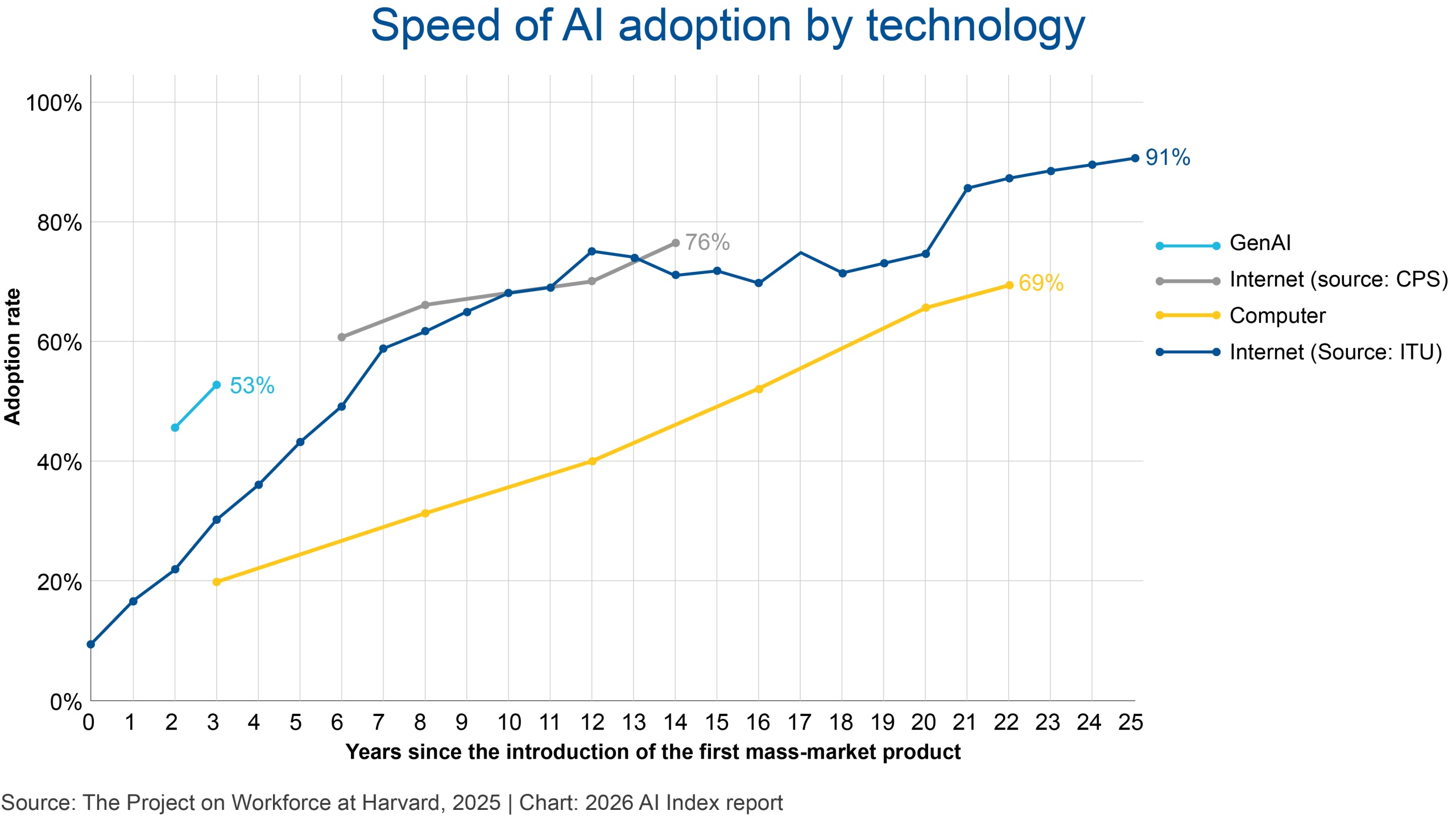

AI is still in the early stages of rapid growth. According to the Stanford AI Index Report 2026, the adoption rate of generative AI reached about 53% within just 3 years of its launch, far exceeding the adoption speed of the internet and personal computers in their time. This also explains the main reason why the AI boom has been so intense over the past three years. Looking ahead, the continuous decline in Token costs driving the popularization of application scenarios has become the core logic for global market investment in AI. In the entire AI industry chain, infrastructure, semiconductors, and end-user applications will all bring significant investment opportunities as adoption rates increase.

Outlook for the Second Half of the Year

Looking ahead to the second half of 2026, the deepening implementation of AI applications will become the market focus, with the popularity and penetration rate of AI Agents being important indicators to watch. Investors can closely refer to the latest data from platforms like OpenRouter while also paying attention to changes and evolutions in the market's AI narrative.

Furthermore, the capital expenditure intentions of global technology giants in the second half of the year will also be a key variable in the development of the AI story. This is not only a crucial support for the strong performance of the AI infrastructure and semiconductor sectors in the first half but also an important factor influencing market trends in the second half.

Overall, AI remains a key investment theme in the global market in 2026, with its long-term trend of driving economic growth and productivity improvement receiving significant market attention. Sector rotation is expected to accelerate, and divergence is likely to become the norm. Investors should prioritize focusing on leading hardware technology companies with technological barriers and supply chain advantages, while also paying attention to the progress of AI application implementation and flexibly deploying across various segments of the AI industry chain through different ETFs.

In the AI technology race, the following products are worth noting:

- E Fund (Hong Kong) Hong Kong Exchange Tech 100 Index ETF (03456.HK): One-click access to the foundation of China's hardware technology.

- E Fund (Hong Kong) Solactive Asia Semiconductor Select Index ETF (03486.HK): Grasp the computing power key of Asian semiconductors.

- E Fund (Hong Kong) FTSE AI Select Index ETF (03489.HK): Directly target the cutting edge of US-China AI transformation.

Important Information

The issuer of this content is E Fund Management (Hong Kong) Limited. This content is for reference only and does not constitute an invitation or recommendation to invest in fund units. This content is for display purposes only and must not be shown to any person to whom such display would be unlawful. Investment involves risks, and you may lose a substantial part of your principal. Before investing, investors should read carefully the investment risks related to the fund in the sales documents (including the "Risk Factors" section). This content has not been reviewed by the Hong Kong Securities and Futures Commission.

For detailed important notices and disclaimers of the above funds, please visit the E Fund (Hong Kong) website: https://www.efunds.com.hk/tc/products/56/important/

https://www.efunds.com.hk/tc/products/53/important/

https://www.efunds.com.hk/tc/products/48/important/

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.