SpaceX: Space Compute — Musk's new hype or real future?

Dolphin Research noted in 'SpaceX: AI Burn Continues, Is 'Space Compute Hegemony' the Endgame?' that orbital data centers are not only the core of SpaceX’s grand narrative, but also its largest future 'option value' in valuation.

To realize this vision,$SpaceX(SPCX.US) has laid out an aggressive deployment roadmap for space compute:

1. 2028, first AI compute satellites in orbit: The first AI constellation 'AI1' is slated to start scaled commercial deployment in 2028. These satellites will span up to 70 meters with Avg. power of 120 kW (peak 150 kW), effectively becoming floating power stations in space.

'Starship + in‑house chip fab' as dual engines: From 2028–2031, SpaceX plans two step‑change infrastructure builds: ultra‑high‑frequency heavy‑lift launches via Starship (V3 single‑ship 100 tons to orbit; long‑term goal of 10k units produced and 10k launches per year), and the Terafab chip fab in Texas under SpaceX (2nm process, long‑term output of 1 TW compute capacity, with ~800 GW dedicated to space).

2. Post‑2030, ship 1 mn tons of compute to orbit annually: With launch capacity and silicon supply both ramping, SpaceX targets by 2030–2031 to lift 1 mn tons of compute hardware to orbit each year. At ~100 kW per ton, that implies 100 GW of new space compute deployed annually, with an ultimate target of 1 TW (1,000 GW).

For context, total AI compute deployed on Earth by leading CSPs is only ~30–50 GW. In other words, SpaceX’s annual space compute adds alone could equal two to three times the entire global cloud on Earth. If executed, this would break ground constraints on power and land that cap terrestrial compute growth.

Given the disruptive picture, this note focuses on two questions:

1) Is the leap from ground rehearsal to 'space compute hegemony' sci‑fi, or a dimensionality reduction strike on incumbent tech giants?

2) How should we value SpaceX as a super‑unicorn against such an unprecedented closed‑loop biz. model?

Straight to the analysis:

I. Core question: Can you dump heat in vacuum? Nearly, but not quite

Ground AI data centers are hard enough, while in space the vacuum eliminates convection, leaving only thermal radiation to deep space in IR wavelengths. At the same temperature delta, radiation cooling efficiency is only ~1% of air convection on Earth.

Thermal management is the primary technical bottleneck for space compute, ranking above deployment cost and radiation. In vacuum, getting rid of heat is the physical prerequisite for any compute activity.

SpaceX faces several immediate challenges:

a. Area is hard‑capped: Radiative power scales with temperature, surface area, and emissivity, so higher temp and larger area help. But even at cabinet temps around 70°C, radiative heat rejection maxes at only ~880 W/m².

A 1.5 MW rack would need ~2,100 m² of radiator area (about one‑third of a soccer field), far exceeding fairing volume constraints. This is a fundamental geometry vs. performance trade‑off.

b. Radiator arrays become micro‑debris targets: Large area surfaces are vulnerable, as a 1 mm fragment at orbital velocity can puncture thin radiator walls. LEO satellites also face a 90‑min cycle with temperature swings over 250°C (+120°C to −160°C), inducing severe thermal shock.

Such cycling can crack packages or fatigue coolant lines. With no on‑site repair, a single puncture and fluid loss can zero out cooling and scrap the entire satellite.

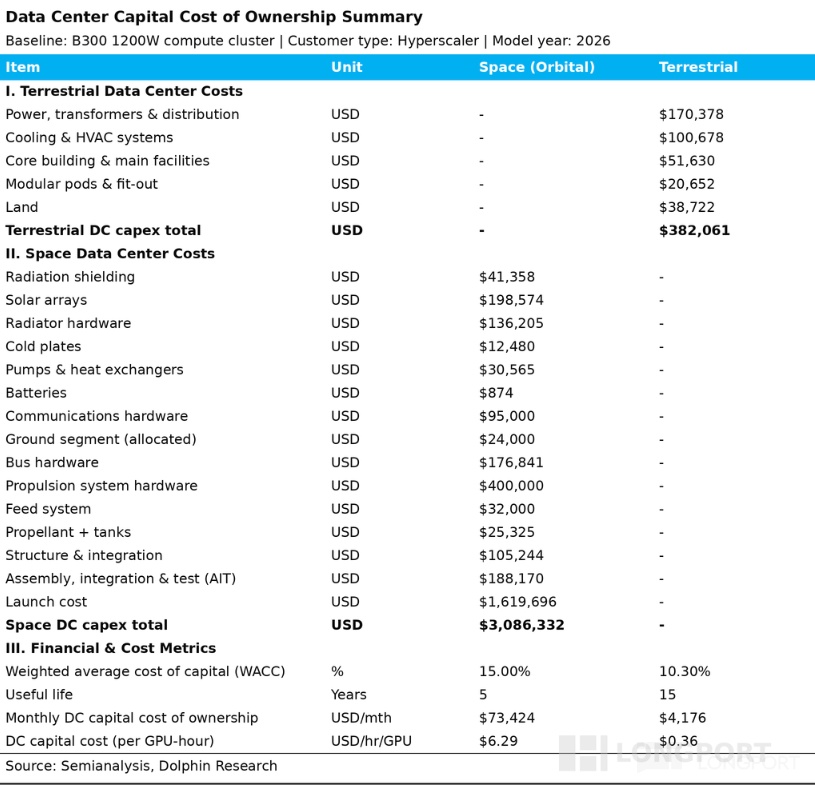

c. High cost: The ISS‑style bespoke approach implies radiator costs of ~$4.5–6.6 mn/kW. Even with commercialized volume learning, bare cooling hardware could still be ~$6 bn/GW, nearly 2x a ground data hall (~$3.3 bn/GW).

d. Freight inversion: On Falcon 9 economics, launch cost to orbit for this 'deadweight cooling' is ~$23 bn/GW, nearly 4x the radiator hardware cost. Even if Starship cuts launch to $200/kg, at 80 W/kg (2026 thermal control), total launch would be ~$2.5 bn/GW.

Only after thermal control improves to ~195 W/kg (2032E) might launch fall toward ~$1 bn/GW. Freight and mass efficiency must improve in tandem to close the loop.

Given the tensions above, space DCs must balance efficiency, mass, and reliability:

a. Trade lifetime for area (raise temp thresholds): Since radiation scales with T⁴, allowing chips to run fully loaded at 85–100°C can cut radiator area by ~15%–25% per +20°C. The trade‑off is reliability, as GPUs/HBM above ~85°C for long periods accelerates failure modes.

b. Trade power for layout freedom (active liquid cooling): Use cold plates → pumps → coolant → external radiators to move heat. This adds ~2%–4% power and pump failure risk, but decouples chip placement from radiator geometry.

c. Trade weight for cost (materials and deployables): Ditch expensive space‑grade alloys for good‑conductivity but heavier 6061‑T6 aluminum, embracing cheap mass for lower manufacturing cost. Fold radiators accordion‑style for launch, then deploy at scale in orbit.

d. Add redundancy to manage risk (modular honeycomb loops): Borrowing from Starlink, use integrated chassis with fins and a modular honeycomb liquid network. On impact, isolate a leaking segment instantly to avoid single‑point failures cascading into total loss.

The active liquid‑cooling plus deployable radiator path is theoretically sound but still at engineering validation stage. It has not been proven at scale in orbit.

II. Space radiation punching through chips? Manageable

In semiconductor physics, a transistor’s radiation susceptibility hinges on 'critical charge' — the minimum energy needed to flip state (0→1). As nodes shrink from 28nm to 3nm and below, device volume and Vdd drop sharply, and critical charge falls exponentially.

High‑energy particles in space can cause SEUs (bit flips) and SELs (latch‑up/burnout). Traditional rad‑hard large‑node chips lack the compute needed for AI, making a pure space‑grade approach impractical.

SpaceX’s approach accepts local errors while protecting system integrity:

a. Orbital advantage: Deploy at 500–1000 km LEO/SSO to leverage Earth’s magnetic field, reducing particle flux at the source. This lowers the error rate before architectural mitigation.

b. Heterogeneous separation: Use 3nm GPUs for compute (cortex), and 65/28nm rad‑tolerant FPGA/MCU for supervision (cerebellum), detecting abnormal currents and power‑cycling GPUs in milliseconds to block permanent damage.

c. Targeted gradient shielding: Avoid full heavy‑metal enclosures. Instead, add ultra‑thin 'low‑Z polymer + high‑Z Ta/W' coatings above GPUs and PMICs to suppress secondary radiation, balancing thermal performance and mass.

d. AI’s natural tolerance plus graded fault tolerance: LLMs are probabilistic; single‑event flips are often acceptable in inference. HBM with ECC self‑corrects, while triple modular redundancy (TMR) on critical control nodes majority‑votes to eliminate hard single‑point errors.

Google’s 67 MeV proton‑beam tests emulating worst‑case LEO conditions challenge the 'must use expensive space‑grade chips' view:

HBM (3x tolerance, silent correction): Errors appeared only after 2 krad, nearly 3x the 5‑yr dose for very low orbits, and all were fixed by ECC with zero service impact. Memory integrity held under aggressive stress.

Compute die (20x tolerance, no physical damage): Withstood 15 krad (~20x expected dose) without permanent damage, keeping AI training and inference stable. This validates COTS advanced nodes with software‑level hardening.

In short, 'advanced COTS nodes + ECC/watchdog resets' held up under extreme testing.

III. Latency: a real issue

Inside, a space DC still looks like a standard 'NVIDIA room', but the outside fabric is a vast wireless mesh of space lasers (inter‑satellite) and microwave/laser hybrids (space‑to‑ground):

a. Inside a satellite vs. inside a rack: same GPUs on the same board still use NVLink/NVSwitch. Nodes still connect over Ethernet or InfiniBand for the local network.

b. Node‑to‑node (satellite vs. building): from physical to invisible On Earth, rooms/racks interconnect via buried or aerial fiber. In space, cabling disappears, replaced by optical ISLs — invisible laser beams for ultra‑fast links.

c. Backbone return (space‑to‑ground vs. terrestrial backbone): stability vs. speed This is the biggest gap. Terrestrial DCs plug into ultra‑stable, ultra‑high‑bandwidth fiber backbones, while space compute must traverse the atmosphere to reach users, forcing physical compromises.

For stability (Ka‑band microwave): Today’s mainline option transmits at ~17 Gbps, slower but rugged, weather‑proof, and truly 24/7. Reliability trumps peak speed in many ops scenarios.

For speed (optical ground links): The upgrade path offers 100x bandwidth, ideal for AI bulk data. But it is weather‑sensitive, dropping in clouds and rain, and requires dense global ground stations, adding cost and operational complexity.

Current issues for space DCs include:

a. Data latency: A LEO compute satellite orbits ~15x/day, with only 5–7 minutes over a given ground site per pass. Quality is best only when the satellite is over the nearest ground station, which occurs for just 5–7 minutes daily.

Once it moves on, data must hop across multiple satellites like a relay game, pushing one‑way latency to ~30–80 ms (vs. <1 ms over fiber). Multi‑hop routing is inherent to the architecture.

b. Space‑to‑ground return: Switching to optical ground links worsens the issue. Weather‑driven outages require a massive, globally redundant ground network, and the backhaul from dispersed stations to end users adds more latency.

Feasible approaches for SpaceX include:

b. Push 'sense‑compute integration' at the edge: Let imaging satellites hand off to nearby compute birds, run on‑orbit AI in ~1s, then transmit only compressed conclusions in kilobytes (e.g., 'anomaly at lat/long X') instead of 10 GB raw images.

With downlink volumes cut by >90%, the system can fall back to weather‑proof microwave (Ka/V) when lasers are down and still respond within seconds. The trade‑off is degraded multi‑turn, multimodal interactive AI experiences.

Since latency is bounded by light speed and orbital mechanics, it cannot be engineered away. Space DCs must forgo millisecond real‑time uses (autonomous driving, HFT) and target async workloads with high latency tolerance: AI training (days/weeks), weather/climate modeling (seconds acceptable), and in‑situ space compute (debris warnings, astrophysics).

Operations & maintenance: Lack of easy on‑orbit manual intervention is core O&M risk. For now, redundancy (e.g., pre‑provision ~20% surplus GPUs to offset permanent failures and radiation‑driven availability loss, say 95% compute availability) and software fault tolerance (ECC, watchdog resets) stand in for field repair, raising TCO.

Space robotics remain experimental, but post‑2032, on‑orbit robots should mature to enable some repair and swaps. That would extend the service life of space DCs.

IV. Unit economics: does it pencil?

Above we assessed technical feasibility. Now the economics: vs. terrestrial DCs, space DCs lean on near‑unlimited energy.

But that energy is not free. Different orbits have very different sun exposure, directly driving power availability and storage cost:

LEO: About 15 orbits/day with only ~60% in sunlight on Avg., leading to lower effective irradiance and frequent eclipses. Large batteries are needed, raising system complexity and capex meaningfully.

Dawn‑dusk SSO: The preferred orbit for space DCs runs retrograde along the terminator, staying sun‑facing most of the year. Daily shadow lasts up to 35 minutes, so storage needs are far below LEO.

Space DC energy is a capex‑for‑opex substitution: no utility bill, all energy cost is in solar arrays and storage upfront. The essence is not arbitraging scarce electrons, but paying high fixed costs — launch, on‑orbit manufacturing, and reliability — to bypass terrestrial scaling bottlenecks.

Those include power price and interconnect, but also grid interconnection queues, land and permitting, industrial capacity for equipment, and construction labor. Space competes against the full stack of non‑energy constraints on Earth.

On the supply ladder, terrestrial power for compute has four buffer layers, each with distinct costs and scaling friction:

Only after these four layers are progressively exhausted and total terrestrial compute cost keeps rising will space DCs show economic edge. Until then, there is still room to optimize on Earth.

In short, the deciding factor is whether lifetime power‑related opex for ground DCs exceeds the extra non‑energy costs of space compute over its service life. The winner depends on both price paths and timing.

From this, two distinct paths emerge for space compute: 'nice‑to‑have' vs. 'must‑have'

1) Power supply/demand normalizes

Cost dynamics: from prohibitive to long‑term parity

Initial disadvantage (2026): Space DC TCO is >4x terrestrial. Costs stem from custom rad/cooling hardware, shorter chip life under heat/radiation (5 yrs vs. 15 yrs), radiation reducing usable compute (95%), and high redundancy to offset non‑repairability (~20% GPU over‑provision).

Parity over time (2040): As thermal and radiation engineering hurdles are solved and Starship slashes launch costs, LCOC for space vs. ground converges around 2040. In fact by early 2030s, space could be only ~30% above ground, near scale thresholds.

b. Supply/demand: ample terrestrial power, space is optional

In the base case, the four terrestrial layers unlock smoothly, expanding available data center power from 89 GW in 2026 to 338 GW by 2030. The market absorbs demand without forcing a shift to orbit.

2) Severe bottlenecks in terrestrial power expansion ('power crunch')

a. Cost scissors: parity arrives 6 years earlier

Ground costs spike: Grid approvals plus shortages of gas turbines and transformers drive terrestrial DC capex from $34.6 mn/MW to $53.4 mn/MW in the stress case. This resets the baseline higher for years.

Space costs plunge: Starship drives launch to ~$80/kg with scale effects, cutting space DC capex to ~$11 mn/MW. Space LCOC reaches parity around 2034, ~6 years earlier than base case.

Beyond parity, space keeps widening its cost edge, with LCOC ~20% below ground by 2039. That establishes a durable competitive position for orbit‑based compute.

b. Supply/demand: the tipping point — 'space overflow' from compute supercycle

Chip capacity surges: Terafab adds ~1 mn wafers/month by 2040, lifting the ceiling for deployable compute. On terrestrial power, capacity peaks in 2028 then stays weak.

By 2035, ground DC power reaches only ~576 GW (vs. 1,150 GW in base case), and by 2050 totals ~2,400 GW (vs. ~7,500 GW). The binding constraint flips from chips to power on Earth.

Space overflow triggers: Although LCOC parity arrives in 2034, actual demand spillover starts in 2037 when chip output blows past the ground power ceiling. The compute gap is forced into orbit.

As demand compounds, space compute scales fast: ~200 GW in orbit by 2038, soaring to ~4,800 GW by 2050, or ~73% of chip output. Space becomes the primary, near‑only viable deployment surface for AI at scale.

V. How to value SpaceX, the giant?

① Launch services: In 'From Daydream to Fortune, Is SpaceX Really That Sci‑Fi?', Dolphin Research viewed launch as near‑absolute monopoly, sometimes likened to the East India Company of the Age of Sail.

For such a unique monopoly asset, our approach: If the 1 mn‑ton annual lift fully materializes and is priced at $200/kg on a market basis, Starship’s long‑term annual revenue would be ~$200 bn. After the early R&D/test phase, using Falcon 9’s mature ~30% EBITDA margin as proxy, annual EBITDA would be ~$60 bn.

As 'high‑tech infra logistics' with massive physical moats, we benchmark mature heavy‑asset cross‑border logistics peers and apply 10x EV/EBITDA. That yields an enterprise value ceiling of ~$600 bn for launch alone.

Discounted at a 10.3% WACC to present, the implied market value for launch is ~$383.6 bn. This isolates only the launch pillar and excludes other businesses.

② Starlink: In 'SpaceX: Sky Mesh Going Undefeated?', we framed it as a monopolistic space telco nurtured by launch dominance. The core constraint is spectrum spatial reuse.

Terrestrial operators densify cells to reuse spectrum, while one satellite beam covers tens of thousands of square km, forcing all users to share limited capacity. Thus Starlink is complementary, not a substitute, to ground telcos.

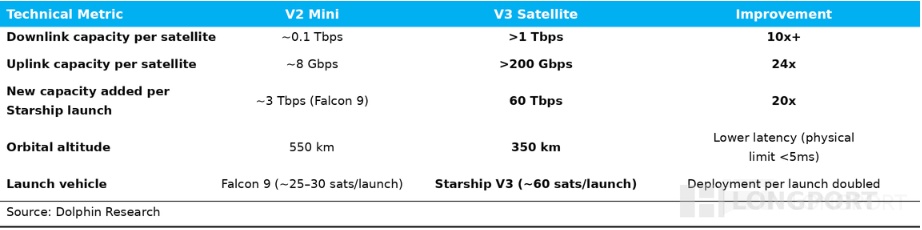

Its core TAM skews to suburbs, remote areas, and air/sea — where terrestrial build‑out is uneconomic — not dense urban cores. SpaceX plans a 42k‑satellite mega‑constellation by 2030 (vs. ~9,600 in orbit now, nearing 10k), spanning V1/V2/V3 and V‑band.

The new V3 satellites are the strategic focus, delivering step‑ups vs. V2 Mini in bandwidth, latency, and architecture. This underpins both consumer broadband and enterprise lines.

a. Broadband: Per ARK Invest, suburban/remote populations total ~3.45 bn (~800 mn households). Even a 42k‑sat V3 constellation (1 Tbps per sat) caps out around 1.63 bn suburban users (~380 mn households) and ~50 mn urban users (~13 mn households) due to physical capacity limits.

Extreme TAM case for modeling: Assume continuous expansion to fully cover 3.45 bn suburban users, with localized pricing pegged at ~2% of regional GNI per household (affordability benchmark). In this end‑state, broadband TAM could reach ~$249.6 bn annual revenue, implying ~$26 monthly ASP per household.

In conversion to revenue, we haircut for non‑universal demand, encroachment from expanding terrestrial edges, and geopolitical blocks in markets like China/Russia. Starlink cannot be winner‑take‑all.

Thus our model assumes: base case 30% share of global suburban market (revenue ~$74.9 bn). In a bull case, scale and first‑mover moats push share to 50% (revenue ~$124.8 bn).

b. DTC to phones: Using 8 bn global mobile devices and ~$8 ARPU for mobile connectivity, the long‑term TAM is ~$740 bn. Given satellite bandwidth limits in dense areas, Starlink’s DTC augments rather than replaces MNOs, via B2B2C revenue sharing.

On the current 55:45 split, Starlink captures a wholesale‑like share rather than full ARPU. For example, Starlink provides the underlying network to a carrier like T‑Mobile US, which bills end users and shares revenue back.

Penetration scenarios: Base case: 10% of 8 bn devices (~800 mn) via value‑added/roaming, at a 55% revenue share implies ~$40.7 bn annual revenue to Starlink. Bull case: 20% penetration (~1.6 bn devices) implies ~$81.4 bn, forming a potent second growth curve.

c. Aviation + maritime:

In enterprise high‑value use, aero and maritime broadband are high‑ARPU, high‑margin: Aviation: ~30k commercial jets at ~$300k annual ARPU imply a ~$9 bn revenue pool. Maritime: ~100k active merchant vessels at ~$34k annual ARPU imply ~$3.4 bn.

Combined TAM is ~$12.4 bn. With LEO advantages in latency, bandwidth, and global coverage, Starlink is rapidly displacing legacy GEO providers.

If Starlink captures 80% of reachable fleets on price/performance, this segment could deliver a stable ~$10 bn high‑margin annual revenue. This would be a durable enterprise pillar.

Across the three pillars, we value Starlink’s 2030 outlook using EV/EBIT with DCF back to 2026:

Base case: 2030 revenue ~$128 bn. With low marginal costs and scale benefits, assume 45% OPM, implying ~$57.6 bn EBIT.

At 15x EV/EBIT (growth telco comp), EV is ~$864 bn in 2030. Discounted at 10.3% WACC, the present fair value is ~$551.2 bn.

Bull case: 2030 revenue ~$218.6 bn. With stronger scale, assume 50% OPM, implying ~$109.3 bn EBIT.

At the same 15x, 2030 EV is ~$1.64 tn. Discounted back, present fair value is ~$1.05 tn.

③ AI: no unique moat

In 'SpaceX: AI Burn Continues, Is 'Space Compute Hegemony' the Endgame?', Dolphin Research defined SpaceX’s AI as X platform, Grok LLM, Colossus ground compute leasing, and orbital DCs. We value each sub‑segment below.

a. X platform

While still being rebuilt, ads fell from a $2.3 bn peak in 2023 to ~$1.8 bn in 2025. X resembles a 'US‑Weibo': still central during breaking news, but daily commercial traffic and stickiness are eroded by rivals.

Dolphin Research models ad revenue +5% YoY to ~$1.94 bn post‑rebuild. Using 10–15x P/S vs. US comps, X is valued at ~$19.4–29.1 bn.

b. Grok model

With no separate disclosure, we estimate from public data:

Consumer revenue:

1.9 mn SuperGrok users: Using a 3‑tier mix (Lite $9/mo 50%, Standard $28/mo 45%, Heavy $265/mo 5%), weighted ARPU is ~$30/mo. That implies ARR of ~$680 mn.

4.4 mn X Premium users: Subscriptions are primarily social, but include Grok access. Assuming Grok’s incremental value is $8/mo, ARR is ~$420 mn, for total consumer ARR of ~$(1.1) bn.

Enterprise revenue:

Grok Business/Enterprise/API are nascent, with capability gaps limiting enterprise penetration. Assuming 10% of total from B2B, enterprise ARR is ~$100 mn.

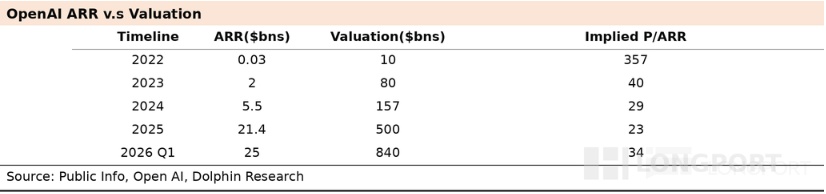

Total Grok ARR is ~$(1.2) bn. Using OpenAI as a reference and Grok’s early growth stage, we apply 50x P/ARR for a base value of ~$60 bn.

If Grok grows ~10% by year‑end (with Grok 5 expected around Jun–Jul 2026, faster Enterprise uptake, and API ramp), ARR could reach ~$2.1 bn. At 35–40x P/ARR, valuation would be ~$74.4–85.0 bn.

c. Ground compute leasing:

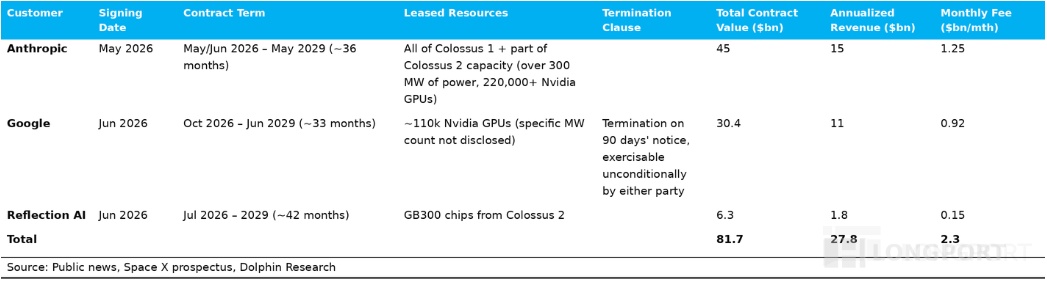

Today SpaceX leases compute to a few mega tenants in single‑tenant hyperscale format. Three signed clients already contribute ~$27.8 bn ARR to SpaceX’s AI segment.

This is highly lucrative — lower‑than‑industry total cost to deploy, yet 3–4x industry pricing power via scarcity and protective terms. That locks in outsized margins vs. peers.

Sustainability is constrained: (i) 90‑day termination makes super‑contracts fragile; (ii) pricing premiums compress as supply/demand normalizes post‑2027/2028. This is a short, scarce window rather than a perpetual line.

Thus near‑term only, we value the $27.8 bn ARR at 3.6–4.5x P/S (CoreWeave/Oracle comps), implying ~$100–125 bn for ground leasing. This frames it as a transient cash‑engine.

d. Orbital data centers:

As above, SpaceX targets 100 GW deployed in orbit annually. Using a current cloud compute leasing benchmark of ~$10 bn/GW, full‑utilization annual revenue could reach ~$1 tn.

Given monopoly‑like, heavy‑asset 'space utility' traits at scale, we assume a 20% steady‑state net margin (net income ~$200 bn) and a conservative 10x P/E. That pegs terminal market value at ~$2 tn for orbital DCs.

Timing varies widely by macro constraints. Using ~10% WACC, we discount back to 2026 under two cases:

Base (optional): If ground power expansion absorbs chip output, space lacks near‑term must‑have status and serves as strategic reserve. Assuming 100 GW deployment is delayed to 2045, the present value is ~$300 bn.

Bull (Musk case): If power crunch intensifies and wafer output breaks ceilings, the 'space overflow' is forced on. Assuming 100 GW deployment by 2035, the present value jumps to ~$814.3 bn on time compression.

Net‑net, orbital DCs are both an engineering feat and a massive call option catalyzed by Earth’s physical constraints — the lower the terrestrial ceiling, the faster SpaceX’s path to trillions.

Rolling up launch (infrastructure logistics), Starlink (space telco), and AI (compute hegemony + LLM), we derive a SOTP‑based fair value for SpaceX today:

<End here>

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.