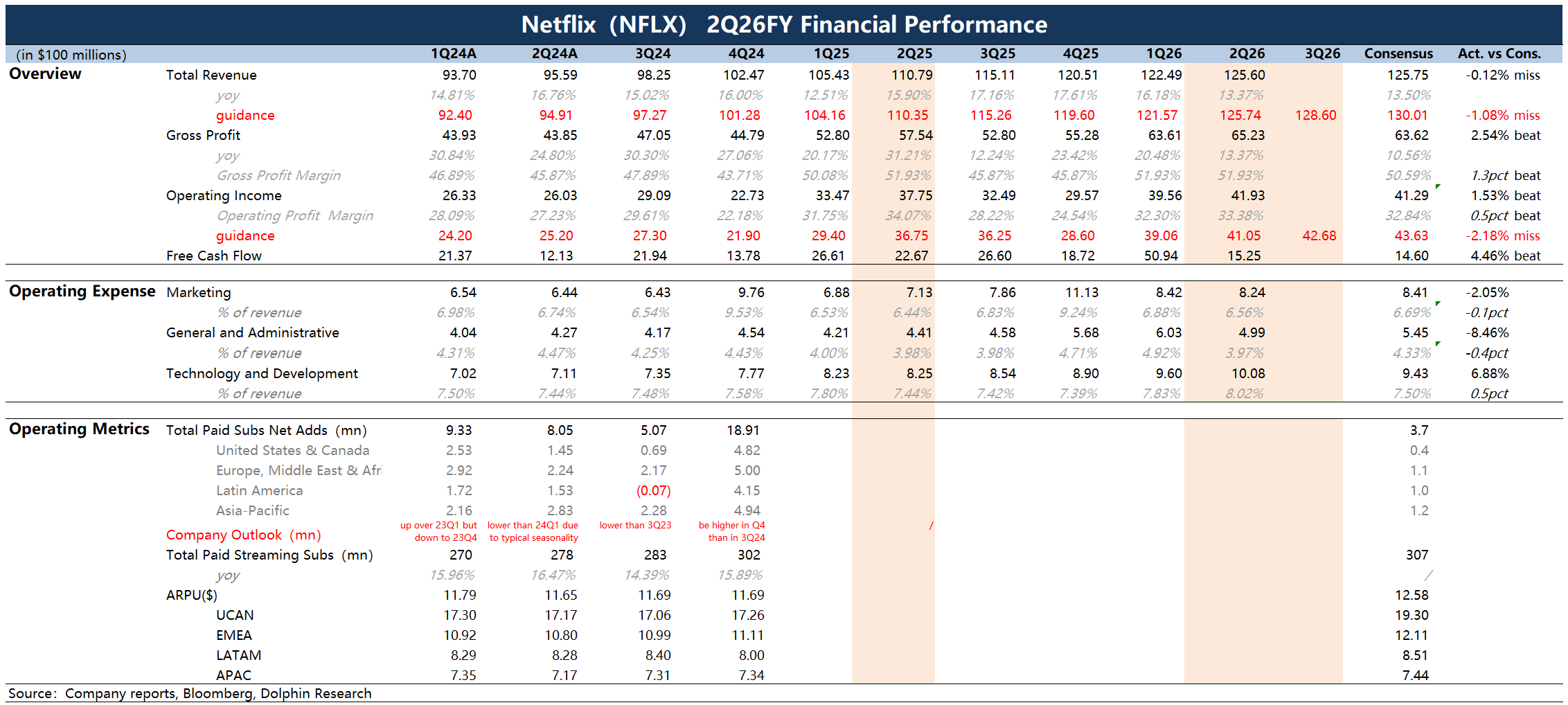

NFLX 2Q26 First Take: Results were lukewarm against modest expectations, with revenue in line with guidance and growth clearly decelerating. The company guided Q3 revenue to $12.86bn, implying further slowdown. NFLX kept its full-year revenue outlook but narrowed the range to $51.0–51.4bn (+13–14% YoY).

Near-term growth softness mainly reflects late-cycle content and the backlash from price hikes in core markets. It also fails to ease investors' medium- to long-term concerns around substitution from short-form video and AI.

The one positive: profitability and cash flow remain relatively stable, even after accounting for a breakup fee on a failed acquisition. This stems from the core business model and potential AI-driven content cost efficiencies.

Beyond that, with the WBD acquisition on hold and a buyback boost announced in Apr., the company repurchased $4.7bn this quarter. This far exceeds its typical quarterly pace in prior years and could continue to help cushion valuation pressure ahead。$Netflix(NFLX.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.