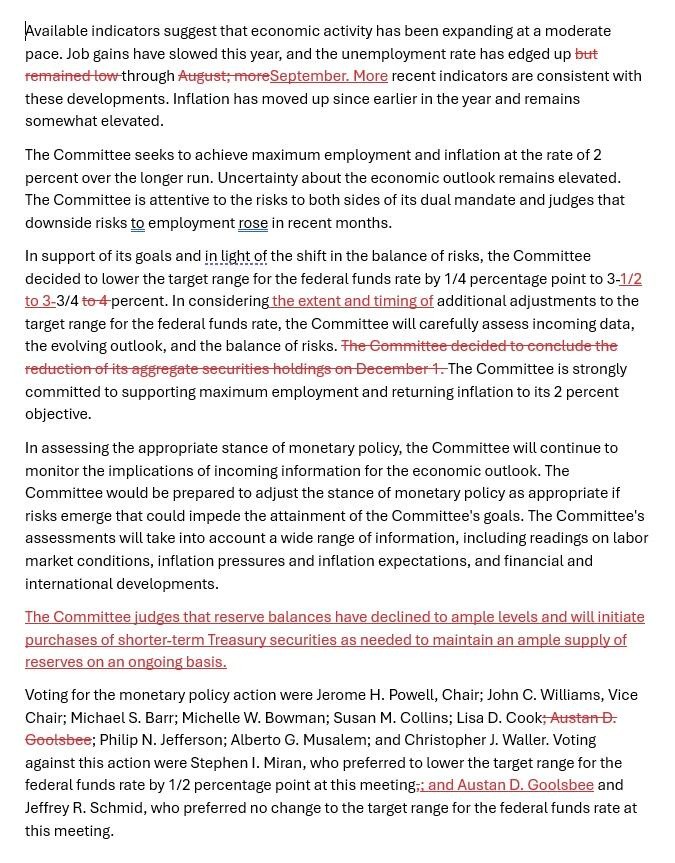

The Federal Reserve lowered interest rates by 25 basis points as expected, but three committee members opposed it. It still anticipates one rate cut next year and will purchase $40 billion in short-term bonds

美聯儲利率決議自 2019 年來首次遭三票反對,一人主張降 50 基點,兩名票委和四名非票委支持按兵不動,實為七人反對決議,分歧據稱為 37 年來最大。會議聲明刪除失業率 “保持低位” ;新增考慮進一步降息的 “幅度和時機”,被視為暗示降息門檻更高。聯儲為維持充足準備金將週五起買短債,預計明年一季度 RMP 購債保持高位。“新美聯儲通訊社”:聯儲暗示可能暫時不會再降息,因內部分歧大得 “罕見”。

要點:

美聯儲如市場所料連續第三次降息 25 個基點,但自 2019 年來首次三票反對利率決議。

特朗普 “欽點” 的理事米蘭繼續主張降息 50 基點,兩名地區聯儲主席以及四名非票委支持按兵不動,實際七人反對決議,據稱分歧為 37 年來最大。

會議聲明重申通脹仍略高企、近幾個月就業下行風險已增加,刪除失業率 “保持低位” 、稱截至 9 月略升。

聲明新增考慮進一步降息的 “幅度和時機”,被視為暗示降息門檻更高。

聲明稱準備金已降至充足水平,為維持充足準備金將本週五開始買短債。紐約聯儲計劃未來 30 天買入 400 億美元短債,預計明年一季度準備金管理購買(RMP)短債保持高位。

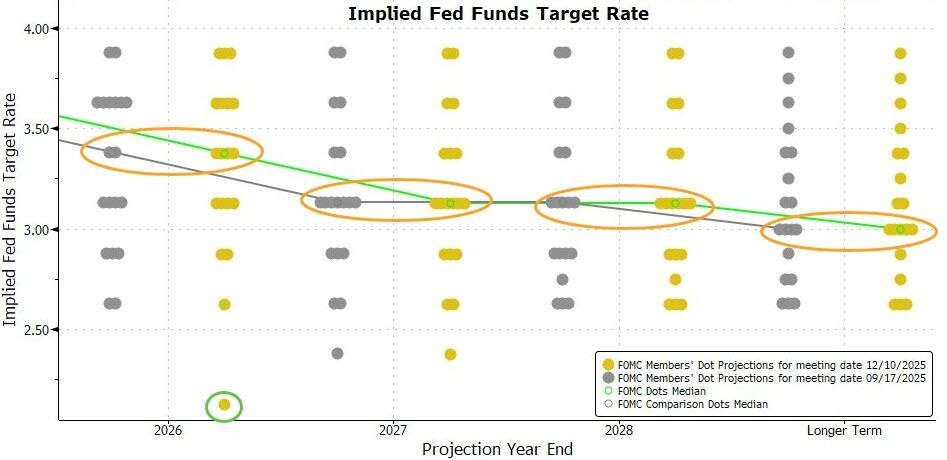

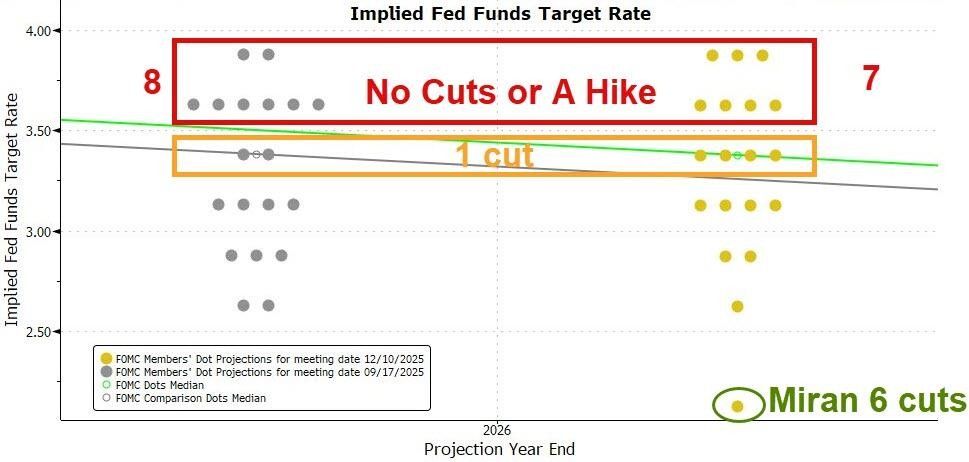

利率預期中位值持平上次,暗示明後年預計各降息一次,點陣圖的明年利率預測變動較上次偏鴿,預計不降息人數少一人至七人。

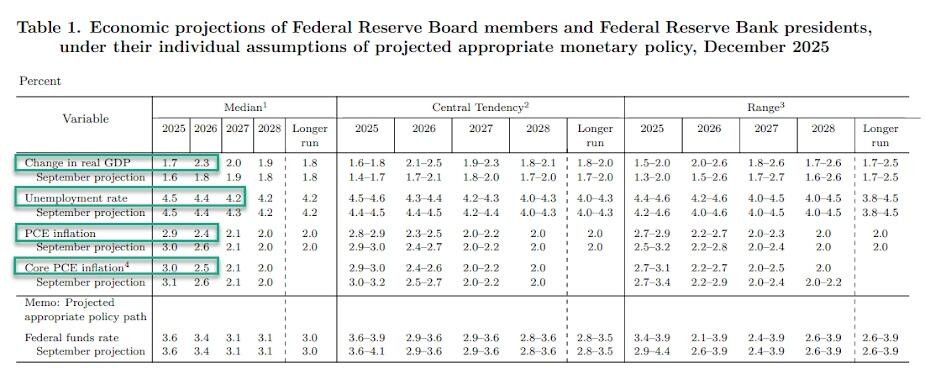

經濟展望上調今年及此後三年 GDP 增長預期,小幅下調今明年通脹和後年失業率預期。

“新美聯儲通訊社”:聯儲暗示可能暫時不會再降息,因內部對通脹和就業擔憂孰輕孰重的分歧大得 “罕見”。

美聯儲如市場所料再次以常規步伐降息,但暴露了投票決策者內部六年來最大的分歧,暗示明年將放慢行動步伐,近期可能不行動。聯儲也如華爾街人士所料啓動準備金管理,決定年末買入短期國債應對貨幣市場的壓力。

美東時間 12 月 10 日週三,美聯儲在貨幣政策委員會 FOMC 會後公佈,聯邦基金利率的目標區間從 3.75% 至 4.00% 下調至 3.50% 至 3.75%。至此,美聯儲連續第三次 FOMC 會議降息,每次均降 25 個基點,今年累計降 75 個基點,自去年 9 月以來,本輪寬鬆週期合計降息 175 個基點。

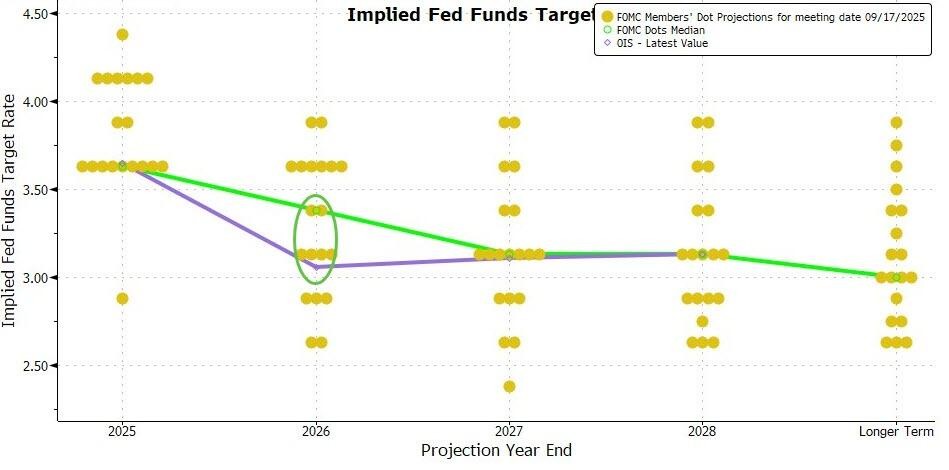

會後公佈的點陣圖顯示,美聯儲決策層的利率路徑預測和三個月前公佈點陣圖時一致,依然預計明年會有一次 25 個基點的降息。這意味着,明年的降息動作將較今年明顯放緩。

本次降息和暗示明年行動放緩幾乎完全在市場意料之中。到本週二收盤,芝商所(CME)工具顯示,期貨市場預計本週降息 25 基點的概率接近 88%,而接下來再降息至少 25 基點的概率到明年 6 月才達到 71%,明年 1 月、3 月、4 月三次會議這類降幅的概率都未超過 50%。

上述 CME 工具體現的預測可以用近來被熱議的 “鷹派降息” 一詞概括。它是指,美聯儲此次會降息,但同時暗示之後可能暫停行動,近期不會再降息。

有 “新美聯儲通訊社” 之稱的資深聯儲報道記者 Nick Timiraos 在聯儲會後發文直言,聯儲 “暗示可能暫時不會再降息”,因為內部就通脹和就業市場哪個更值得擔憂存在 “罕見” 的分歧。

Timiraos 指出,本次會上有三位官員對降息 25 基點持異議,通脹下行停滯不前和就業市場降温導致此次會議成為近些年來分歧最大的一次。

還有評論稱,本次公佈的點陣圖顯示,包括兩名投票 FOMC 委員在內,共六人預計 12 月不降息,換句話説共七人反對本次降息 25 基點,以這一人數看,本次的分歧為 37 年來最大。

2019 年來首次三票反對利率決議

相比 10 月末的上次會後決議,本次會議聲明最大的區別是,在 12 名 FOMC 投票委員中,共有三人投票反對本次降息 25 個基點,反對票比 10 月末的上次會議多一票。這是自 2019 年來首次美聯儲利率決議遭到三名投票委員反對。

聲明顯示,包括美聯儲主席鮑威爾、此前被美國總統特朗普公開放話解僱的聯儲理事庫克在內,共有九名 FOMC 成員支持繼續降息 25 個基點。投反對票的三人分別是,特朗普今年 “欽點” 的美聯儲理事米蘭(Stephen Miran)、芝加哥聯儲主席古爾斯比(Austan Goolsbee)和堪薩斯城聯儲主席施密德(Jeffrey Schmid)。

其中,米蘭和他上任以來出席的前兩次會議一樣,一直希望降息 50 個基點。施密德和上次會議一樣,持異議是因為他支持保持利率不變。上次支持降息 25 基點的古爾斯比這次轉變立場,和施密德站在同一陣營。

今年美聯儲已有四次 FOMC 會議的決議出現了反對票。7 月和上次會議都有兩名 FOMC 票委反對,9 月的會議僅米蘭一人反對。

這些投票分歧體現出,在政府關門導致一些官方數據不能及時披露甚至永久缺失的情況下,美聯儲決策者對通脹和就業的風險權衡並不統一。反對降息者主要擔心通脹下行的進展停滯,支持降息者則認為,應該繼續行動避免就業加速流失、勞動力市場形勢惡化。

新增考慮進一步降息 “幅度和時機”

本次會議聲明相比上次的另一個主要變動體現在利率指引。雖然本次決定降息,但聲明不再籠統地説,在考慮進一步降息時,FOMC 將評估未來的數據、持續變化的前景和風險平衡,而是更明確考慮降息的 “幅度和時機”。聲明改稱:

“在考慮對聯邦基金利率目標區間進行進一步調整的幅度和時機時,(FOMC)委員會將仔細評估最新數據、不斷變化的(經濟)前景以及風險平衡。”

緊接着上面這句話,聯儲聲明繼續重申,堅定致力於支持充分就業,以及讓通脹率回落聯儲的目標水平 2%。

這和華爾街人士此前預計的調整一致。他們預計聲明會迴歸一年前的風格,重新使用 “進一步調整的幅度和時機” 這種措辭。高盛認為,這樣調整反映出,“任何進一步降息的門檻都會更高”。還有評論稱,考慮 “幅度和時機” 是去年 12 月的聲明措辭,被視為暫停行動的信號。

刪除失業率 “保持低位” 稱截至 9 月略升

聲明中其他有關經濟的評價大多沿用了上次聲明的説辭,為了體現官方數據不足的影響,重申“可獲得的指標顯示,經濟活動擴張速度緩和”。

聲明重申,今年就業增長已放緩,對失業率的表述略有調整。上次説 “失業率略有攀升,但截至 8 月仍保持低位”,這次改為 “失業率截至 9 月略為攀升”,刪除了 “保持低位”。緊接着這些説辭,聲明稱,更近期指標也與這些趨勢相符,重申通脹率自年初以來有所上升,依舊略為高企。

和上次一樣,本次聲明也説,FOMC“關注其雙重使命所面臨的風險,並判斷近幾個月就業下行風險已增加。”

擬未來 30 天買短債 400 億美元 料明年一季度 RMP 購債保持高位

本次會議聲明相比上次的又一處重要變化是,這次新增了一個段落,特別指出要購買短債,保持銀行體系內充足的準備金供應。聲明寫道:

“(FOMC)委員會認為,準備金餘額已降至充足水平,並將根據需要開始購買短期國債,以此持續維持充足的準備金供應。”

這等於宣佈啓動所謂的準備金管理,為貨幣市場重建流動性緩衝。因為往往年底容易發生市場混亂,銀行通常年底減少回購市場的活動,支持資產負債表應對監管和税務結算。

以下紅字可見本次決議聲明相比上次的刪減和新增內容。

負責公開市場操作的紐約聯儲本週三同步發出公告,稱計劃未來 30 天買入 400 億美元短期國債。

紐約聯儲公告稱,收到 FOMC 的指示,要增加系統公開市場賬户(SOMA)的證券持有量,通過在二級市場購買短期國債、必要時買入剩餘久期最多三年的國債來維持充足的準備金水平。這些準備金管理購買(RMP)的規模將根據對美聯儲負債需求的預期趨勢以及季節性波動、例如納税日影響的波動進行調整。

公告寫道:

“月度 RMP 金額將在每月第九個工作日左右公佈,同時還會公佈接下來約 30 天的暫定購買計劃。交易台計劃於 2025 年 12 月 11 日公佈首份計劃,屆時 RMP 的短期國債總額約為 400 億美元,將於 2025 年 12 月 12 日開始購買。

交易台預計,為抵消(明年)4 月非準備金負債預計大幅增加的影響,RMP 的(購買)將在未來幾個月內保持較高水平。此後,總購買速度可能會根據美聯儲負債的預期季節性變化而大幅放緩。購買金額將根據準備金供應前景和市場狀況進行適當調整。”

點陣圖顯示本次決議反對者七人 明年利率預測變動較上次偏鴿

本週三會後公佈的美聯儲官員利率預測中位值顯示,聯儲官員本次的預期和 9 月公佈的上次預測一模一樣。具體預測的中位值如下:

2026 年底的聯邦基金利率為 3.4%,2027 年底聯邦基金利率為 3.1%,2028 年底聯邦基金利率 3.1%,更長期的聯邦基金利率為 3.0%,均持平 9 月預期。

以上述利率中位值計算,和上次一樣,美聯儲官員目前也預計,在今年降息三次後,明年和後年大概各會有一次 25 個基點的降息。

點陣圖顯示,此次有六人預計今年末利率在 3.75% 到 4.0%,佔提供預測總人數的 30% 以上。這相當於,共六人認為本次會議應保持利率不變,其中包括有 FOMC 會議投票權的兩名投反對票票委,以及四名沒有此次會議投票權的聯儲官員。加上力主更大幅降息的理事米蘭在內,反對本次會議降息 25 基點的總人數就達到七人。

之前不少人預計,點陣圖反映的未來利率變動將顯示聯儲官員更偏鷹派。本次的點陣圖並沒有這種傾向,反而相比上次偏鴿派。

在19 名提供預測的聯儲官員中,本次有七人預計明年利率在 3.5% 至 4.0% 之間,上次這樣預測的有八人。這意味着,預計明年不降息的人數比上次少一人。

點陣圖還顯示,本次有八人預計利率在 3.0% 到 3.5% 之間,比上次這樣預測的人數多兩人。本次有三人預測明年利率在 2.5% 到 3.0%,比上次少兩人,本次有一人預測利率低於 2.25%,上次無人這樣預測。

上調四年 GDP 增長預期 小幅下調今明年通脹和後年失業率預期

會後公佈的經濟展望顯示,美聯儲官員本次上調了今年以及此後三年的 GDP 增長預期,其中明年的增速上調幅度最大、提高 0.5 個百分點,其他年份均僅小幅提高 0.1 個百分點,小幅下調了 2027 年、即後年的失業率預期 0.1 個百分點,其餘年份失業率預期均保持不變。這種調整顯示,美聯儲認為勞動力市場更具韌性。

同時,美聯儲官員小幅下調了今明兩年的 PCE 通脹以及核心 PCE通脹預期各 0.1 個百分點。這體現出,美聯儲對未來一段時間內通脹放緩的信心略有增強。

和上次一樣,聯儲官員依然預計,到 2028 年,通脹回落至聯儲的長期目標水平 2%,那將是美國通脹率在連續七年高於聯儲的目標後首次達標。

具體預測如下:

- 2025 年的 GDP 預期增速為 1.7%,9 月預期增速 1.6%,2026 年預計增速為 2.3%,9 月預計為 1.8%,2027 年預期增速 2.0%,9 月預期 1.9%,2028 年預計增速 1.9%,9 月預期 1.8%,更長期預期增速為 1.8%,持平 9 月預期。

- 2025 年的失業率預期為 4.5%,2016 年的預期為 4.4%,均持平 9 月預期,2027 年的預期為 4.2%,9 月預期 4.3%,2028 年和更長期的失業率預期均為 4.2%,均持平 9 月預期。

- 2025 年 PCE 通脹率預期為 2.9%,9 月預期 3.0%,2026 年預期為 2.4%,9 月預期 2.6%,2027 年增速預期為 2.1%,2028 年和更長期的預期均為 2.0%,均持平 9 月預期。

- 2025 年核心 PCE 預期為 3.0%,9 月預期 3.1%,2026 年的預期為 2.5%,9 月預期 2.6%,2027 年預期為 2.1%,2028 年預計為 2.0%,均持平 9 月預期。