DUOL: Guidance bombs again; is the Green Owl now 'Dead Duo'? ---

$Duolingo(DUOL.US) released Q4 FY2025 results after-hours on Feb 26 (ET). Once again, guidance bombed.

Highlights:

1) Guidance cracked: real slowdown or just conservative?

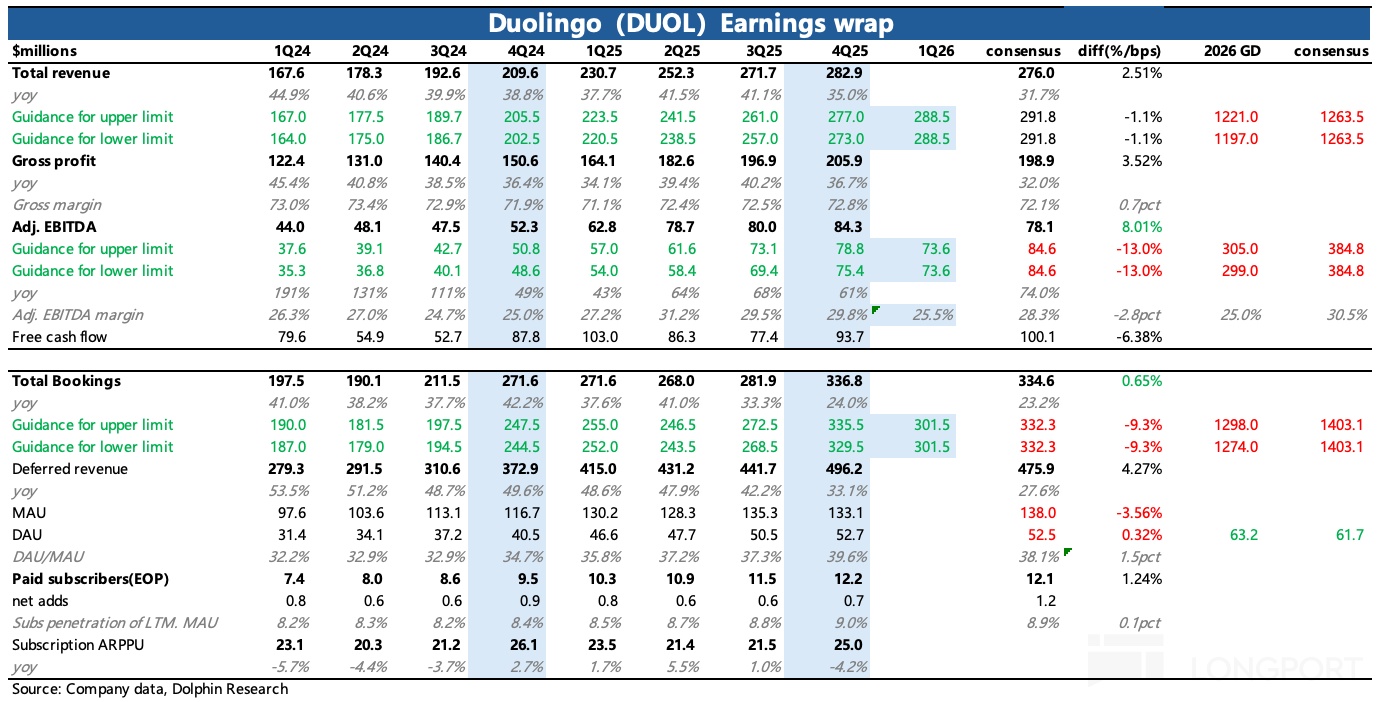

Starting with guidance, management expects Q1 bookings growth of only 11%, with full-year growth at 10–12%. Versus FY2025’s 33%, this is clearly more than natural deceleration. At the same time, the EBITDA margin guide missed and is even guided down ~400bps vs. FY2025.

Regardless of Street expectations, with such a guide and without strong conviction, multiple compression first is a rational market reaction. Some institutions trimmed expectations ahead of the print, yet the actual guide came in even more conservative. That amplified the de-rating.

Management has historically guided cautiously, and this round likely includes deliberate conservatism. Even so, a near-term growth target of 10–12% no longer qualifies as high growth.

Conversely, the urgency to invest in new features signals non-transient issues. Reputation damage (the AI-first memo backlash and a failed PR response) and intensifying AI competition both suggest the company needs time to recalibrate.

2) User growth: ~20% near term, double by mid-term

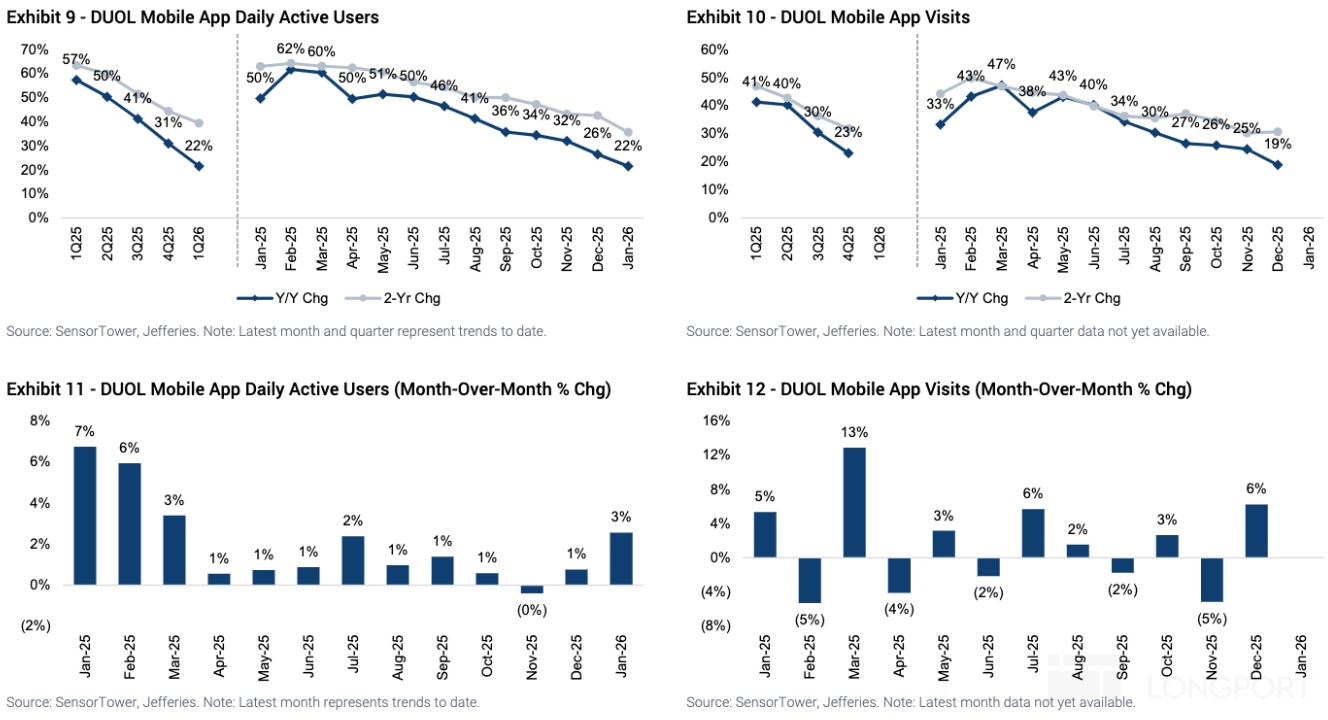

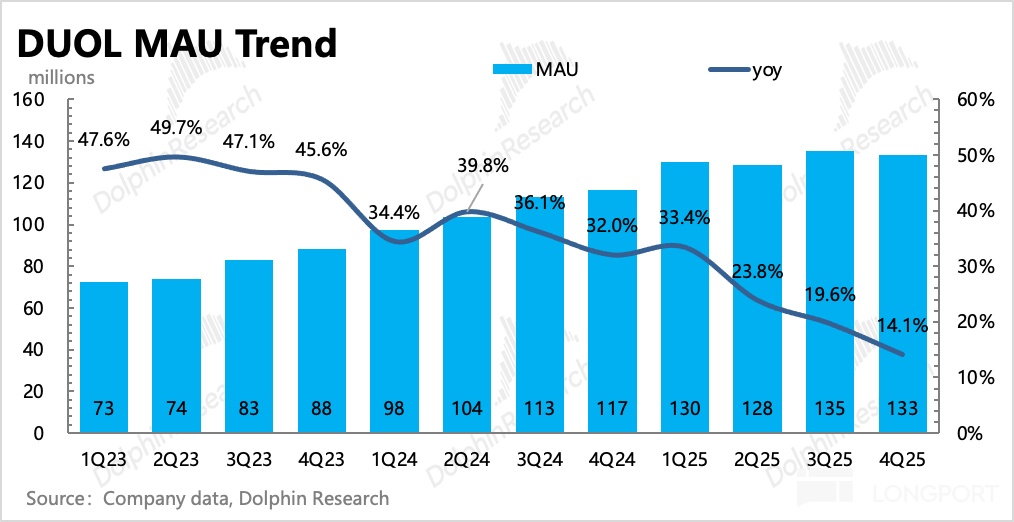

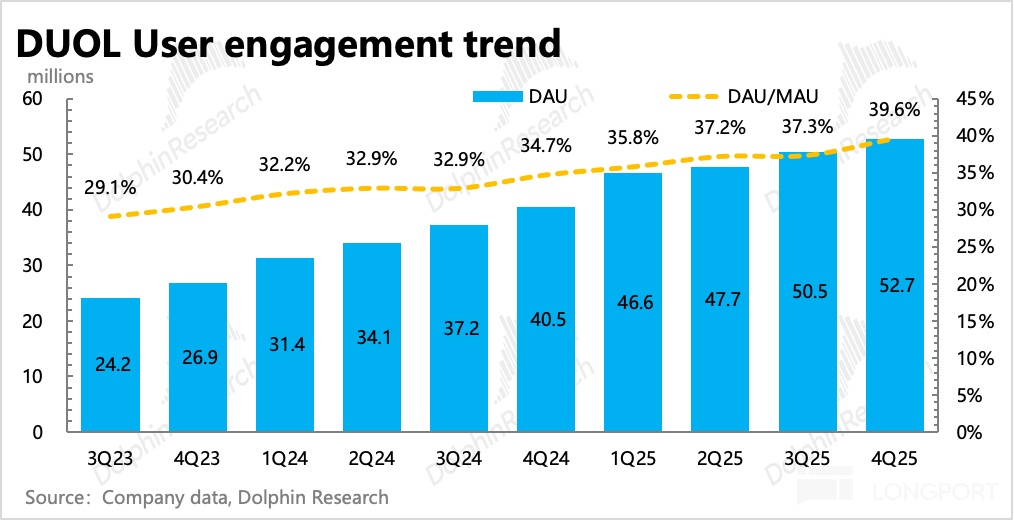

The most-watched user metrics: Q4 MAUs reached 133 mn, DAUs 52.7 mn, with DAU up 30% YoY but slowing QoQ. Sensor Tower shows DAU growth decelerated to 26% in Dec and further to 22% in Jan, driving the YTD share pullback. Momentum eased into the new year.

Per Sensor Tower, growth issues were concentrated in North America and LatAm; in Jan, Duolingo ramped up marketing and ads, largely stabilizing the decline. However, with last year’s 'Dead Duo' campaign ending, Dolphin Research expects Q1 growth to continue slowing overall.

Management set a 2026 DAU growth target of ~20% and remains upbeat on the mid-term outlook through 2028. They believe DAUs can reach 100 mn, roughly double the current scale.

Compared with true utility translation tools, Duolingo still enjoys high stickiness. Q4 DAU/MAU improved to 39%, a high level for any internet platform. If Duolingo can enhance UX through this transition, that could be the key to a comeback.

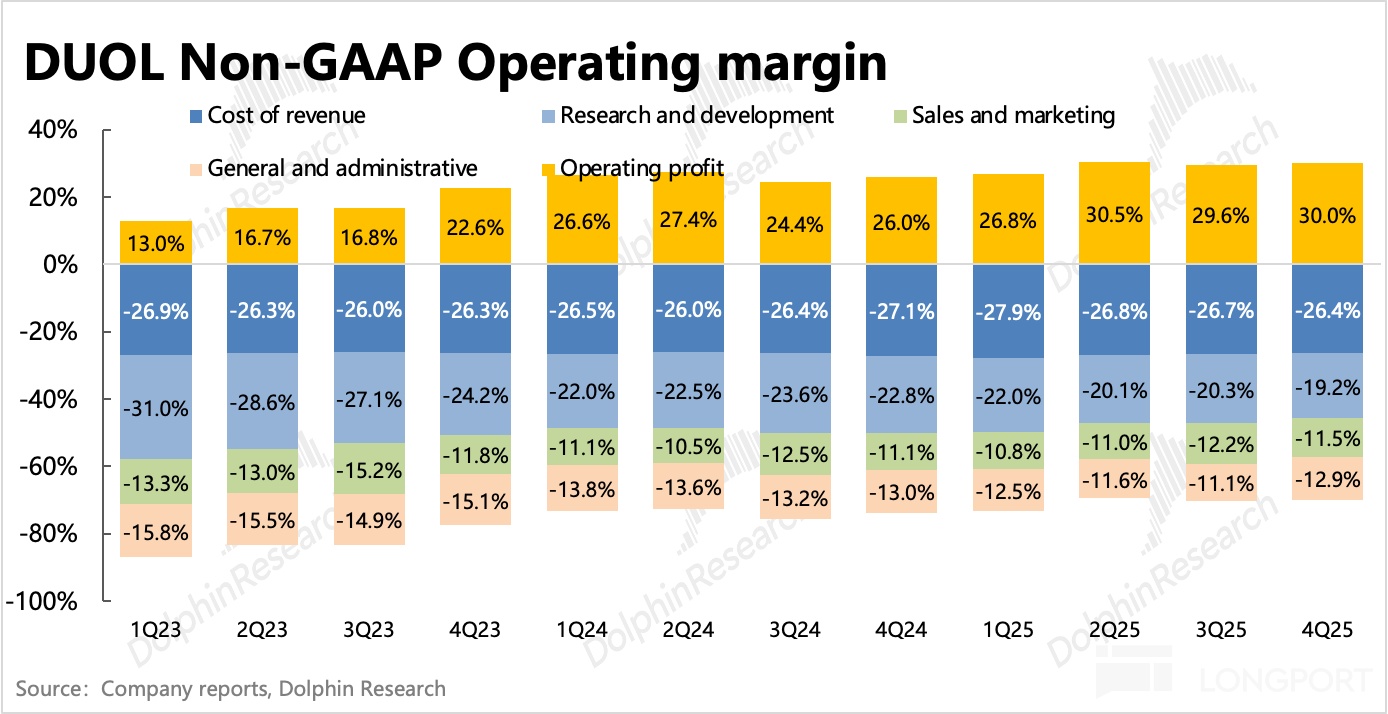

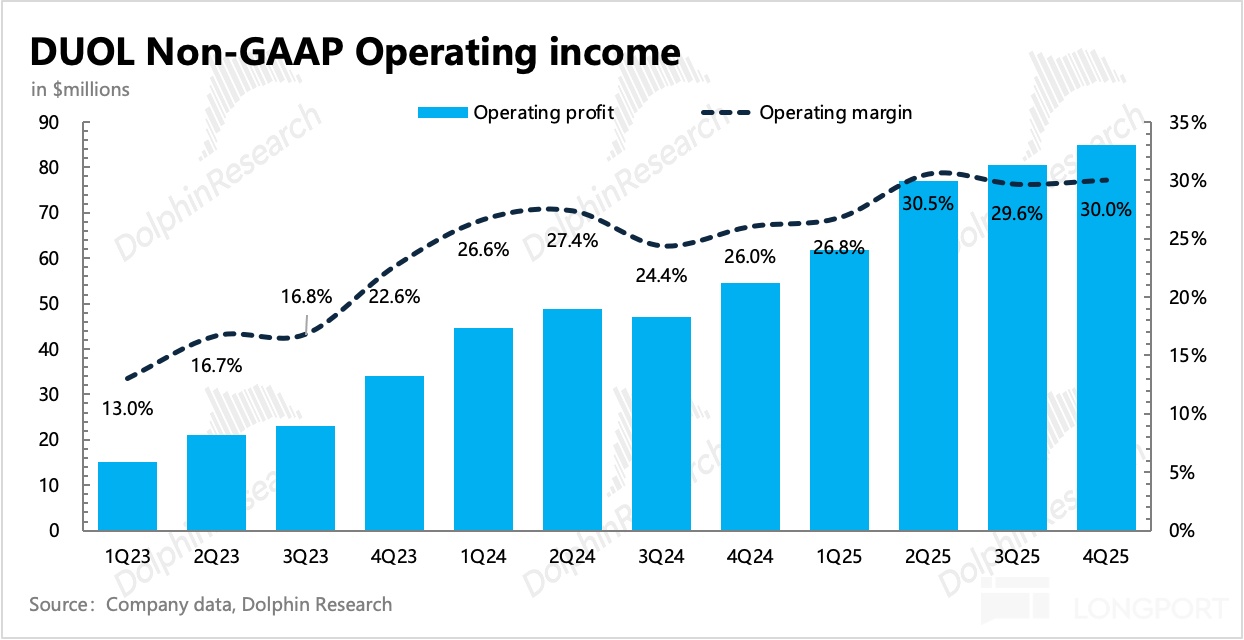

3) Stepping up investment, margins likely to slip Q4 margins held steady, but selling expenses already show early signs of expansion. Management gave a clearer FY2026 profitability guide: with sustained investment in AI features, user acquisition, and high-profile brand marketing, FY2026 gross margin and EBITDA are expected to decline by 200–300bps and 400–500bps vs. FY2025, respectively. Headcount expansion in H1 will also lift SBC-driven dilution to 3–4%, normalizing to ~2% in H2.

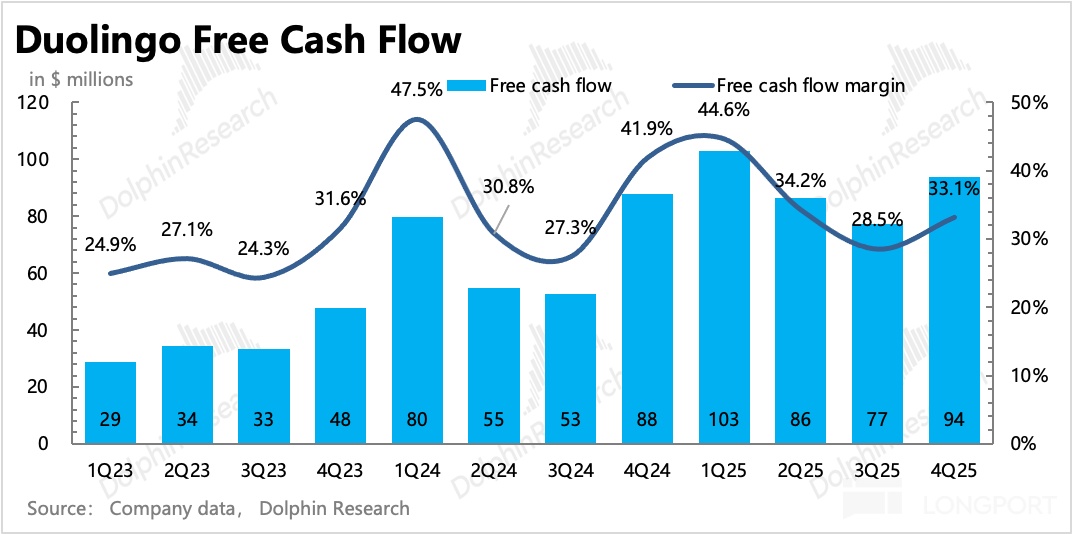

4) FCF and buyback Q4 FCF was $94 mn (33% of revenue), down YoY but up QoQ. Net cash stands at $1.1 bn, and the company approved a $400 mn buyback, though with no specified timetable yet.

5) Key financial metrics at a glance

Dolphin Research View

With slowing user growth and an AI-disruption narrative, coupled with management’s consistent conservatism, bullish sentiment has faded YTD. Even though recent brand pushes (NFL championship weekend) and event marketing (with Bad Bunny) helped user growth recover, the market stayed cautious. The bar was low but not low enough.

Before the print, investors worried the FY2026 guide would be underwhelming, including a cut to prior mid/long-term user growth targets and further margin pressure from heavier investment. Those fears proved justified.

The actual guide was even more conservative, and even the mid-term target to double users failed to restore confidence. Near-term pressures are visible, while a 3-year doubling path looks murky amid multiple challenges. Visibility is limited.

Near term, Duolingo is unlikely to attract aggressive long-only interest; mid-to-long term, a bold reset may be necessary. Facing AI shocks and reputational damage, Duolingo is pursuing self-help: faster product updates, AI enablement, and more marketing to lift stickiness. Execution will be key.

Examples include 'Explain My Answer', word cards, an app logo refresh, a PvP 2-player mode, Super Bowl/NFL ads, and a Bad Bunny-driven Spanish push on social media, plus a renewed viral marketing playbook. These have delivered some initial results. On stickiness, Duolingo is not a pure utility easily displaced by AI; it resembles a leading interactive, content-rich game.

After-hours, the stock fell 20%, putting market cap at ~$4.2 bn. Against the FY2026 guide (implicitly conservative), Non-GAAP EV/EBITDA is ~14x, roughly aligned with the guided growth. If the guide is low or FY2026 is a transition trough, current valuation sits near the bottom range.

From a cash flow standpoint, Duolingo can support ongoing buybacks. But this near-term gray zone is not favored by capital, and sentiment needs time to heal. In the process, a clear DAU inflection post-marketing could be a key catalyst; alternatively, at ~10x EV/EBITDA (~$3 bn), investors may tactically position and wait for stabilization and recovery in user growth.

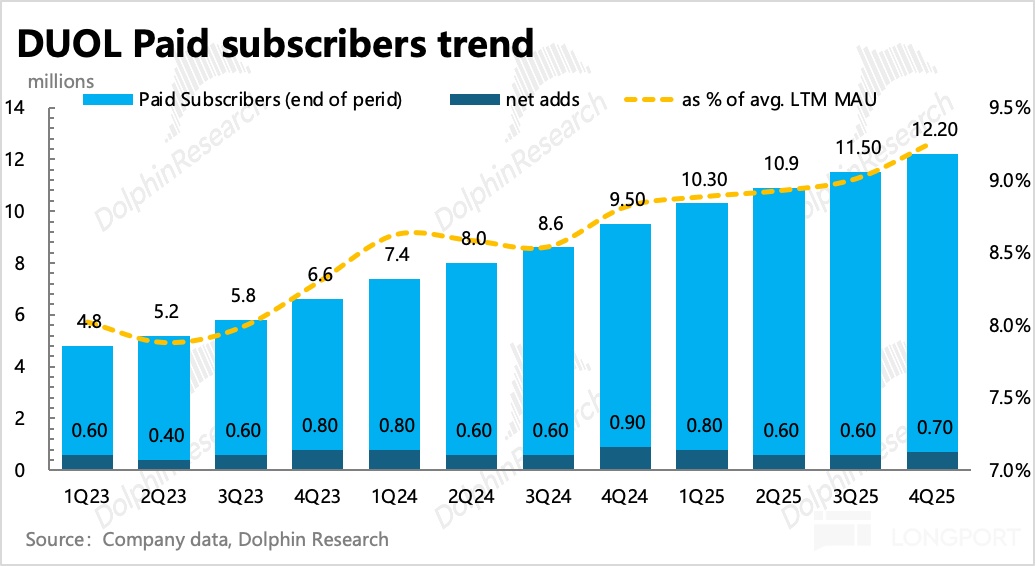

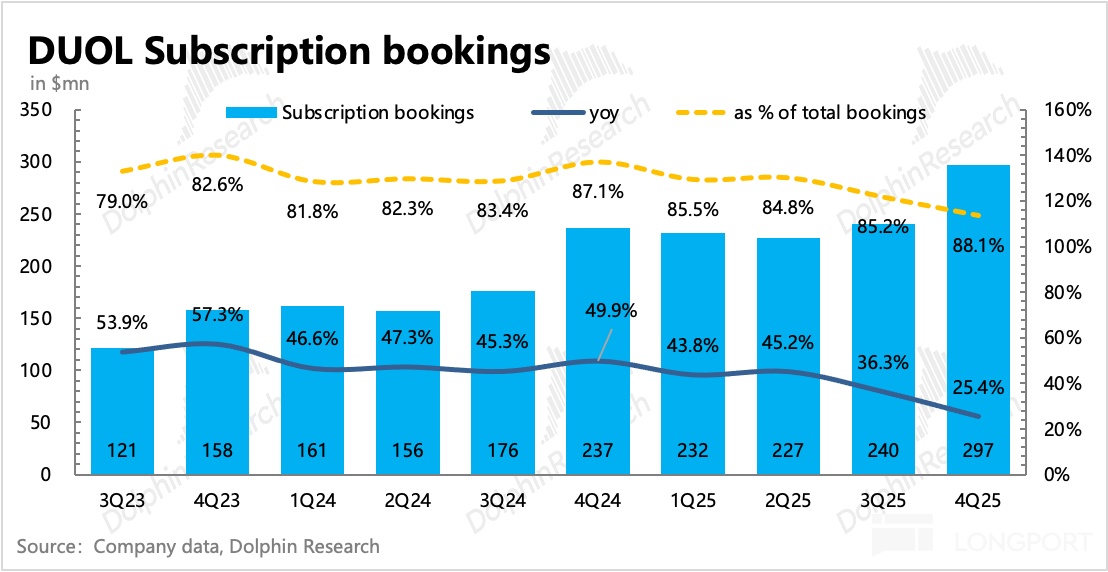

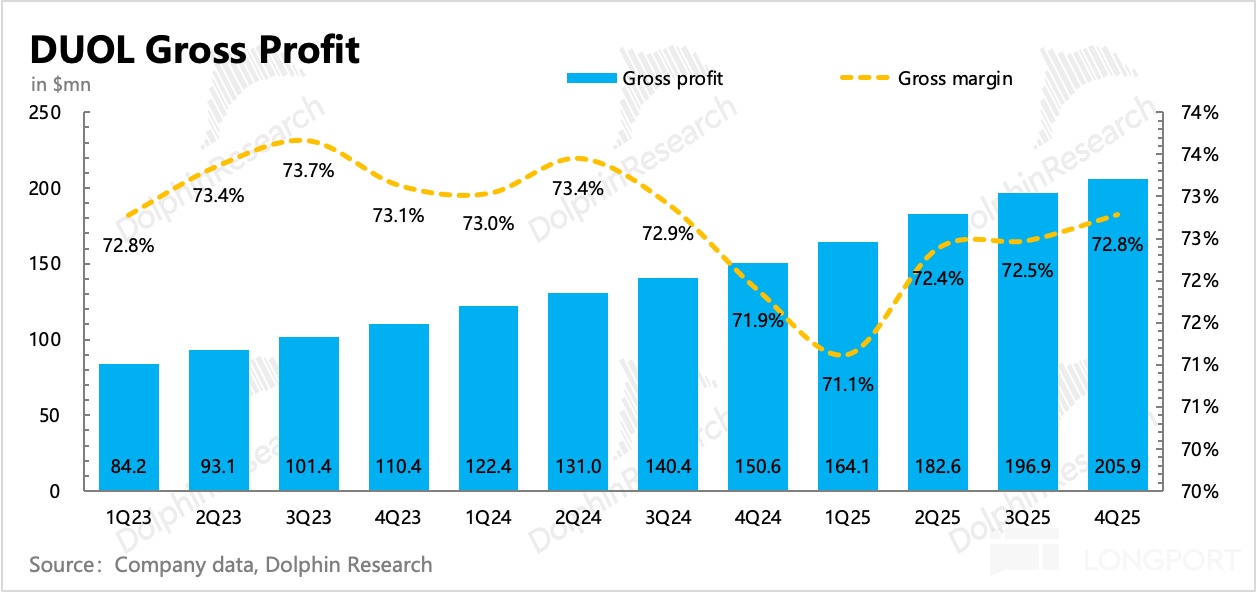

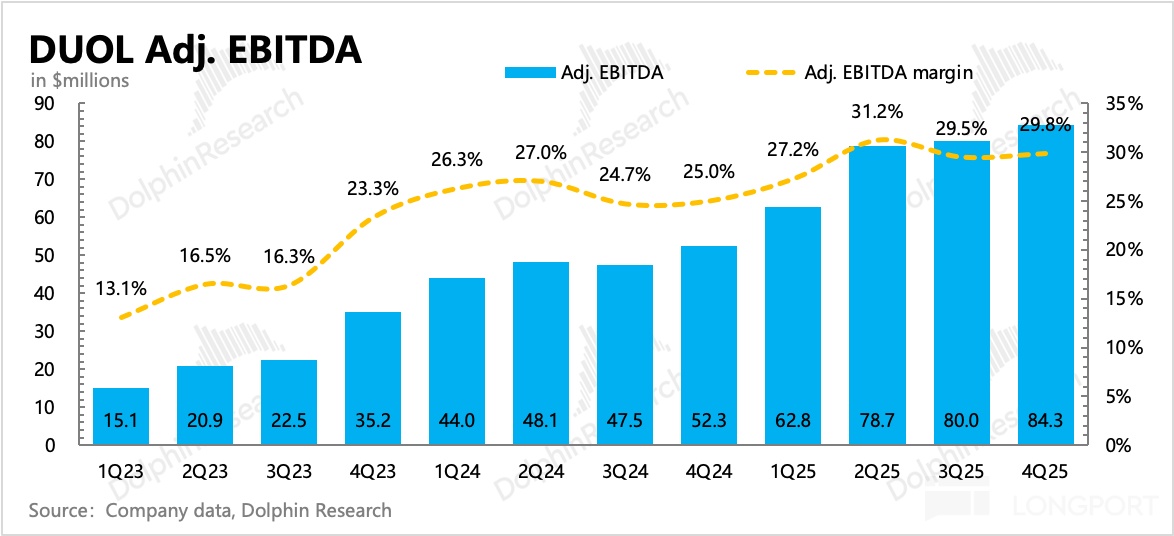

Below are Duolingo’s performance charts:

<End here>

Dolphin Research past pieces on 'Duolingo'

Recent earnings

Nov 6, 2025 call recap ' Duolingo (Trans): Plenty of runway ahead, stepping up to focus on DAU expansion'

Nov 6, 2025 earnings quick take ' Duolingo: The green bird falls from grace'

Risk disclosure and statement: Dolphin Research disclaimer and general disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.